Looking to grow your savings in Malaysia? With the Overnight Policy Rate (OPR) held at 2.75% through the May 2026 Bank Negara meeting, the gap between a lazy 0.25% standard savings account and a well-chosen high-interest account has never mattered more. The biggest shift since this guide was first published is the rise of digital banks (GX Bank, Boost Bank, AEON Bank, Ryt Bank) that now pay 3% to 4% p.a. with little or no hoops, plus conditional “save-spend-invest” accounts from the traditional banks that advertise up to 6.60% p.a. Below is our refreshed June 2026 comparison, with honest notes on which headline rates are realistic and which are marketing.

- Quick Answer: Best Savings Account by Saver Type (2026)

- Full Comparison Table (June 2026)

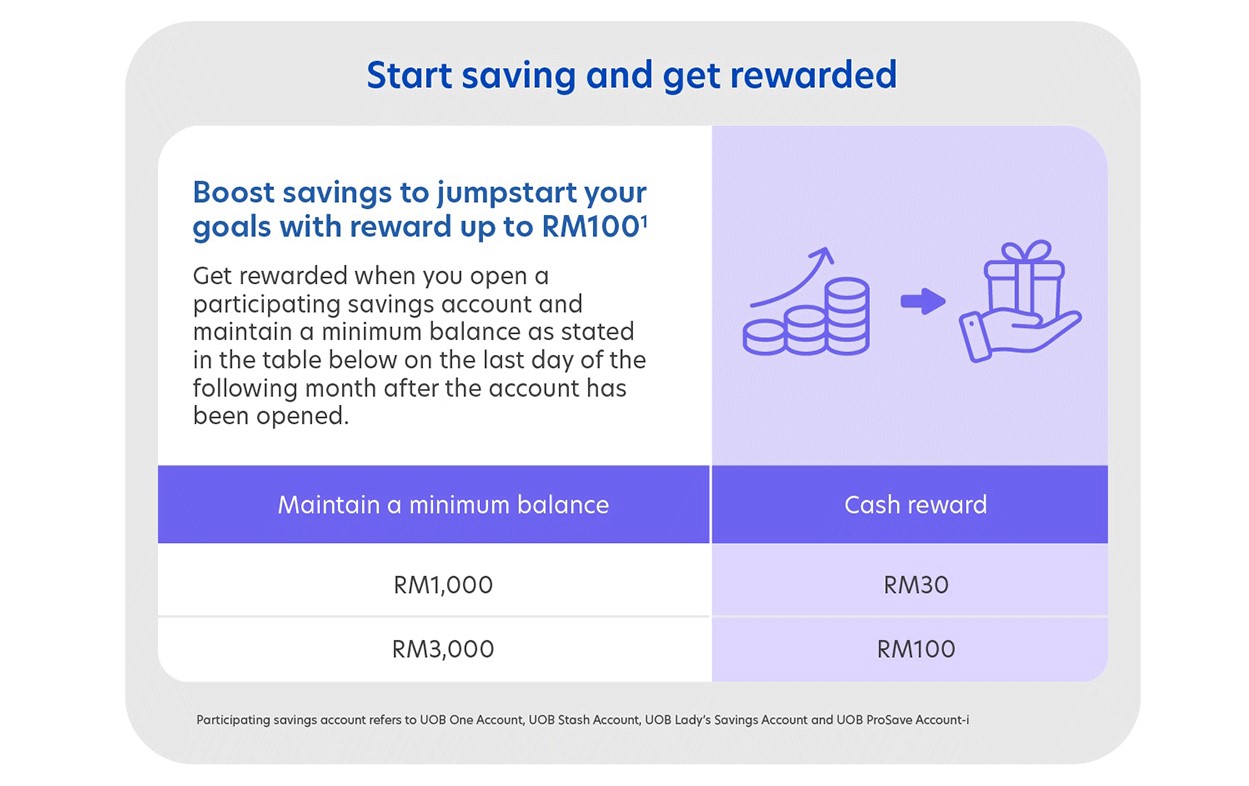

- 1. UOB One Account

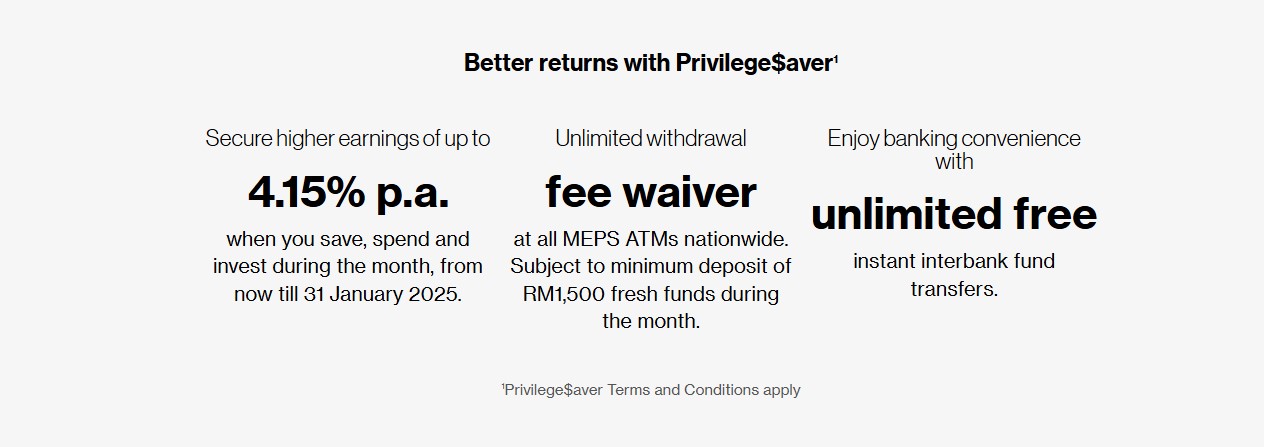

- 2. Standard Chartered Privilege$aver

- 3. RHB Smart Account/-i

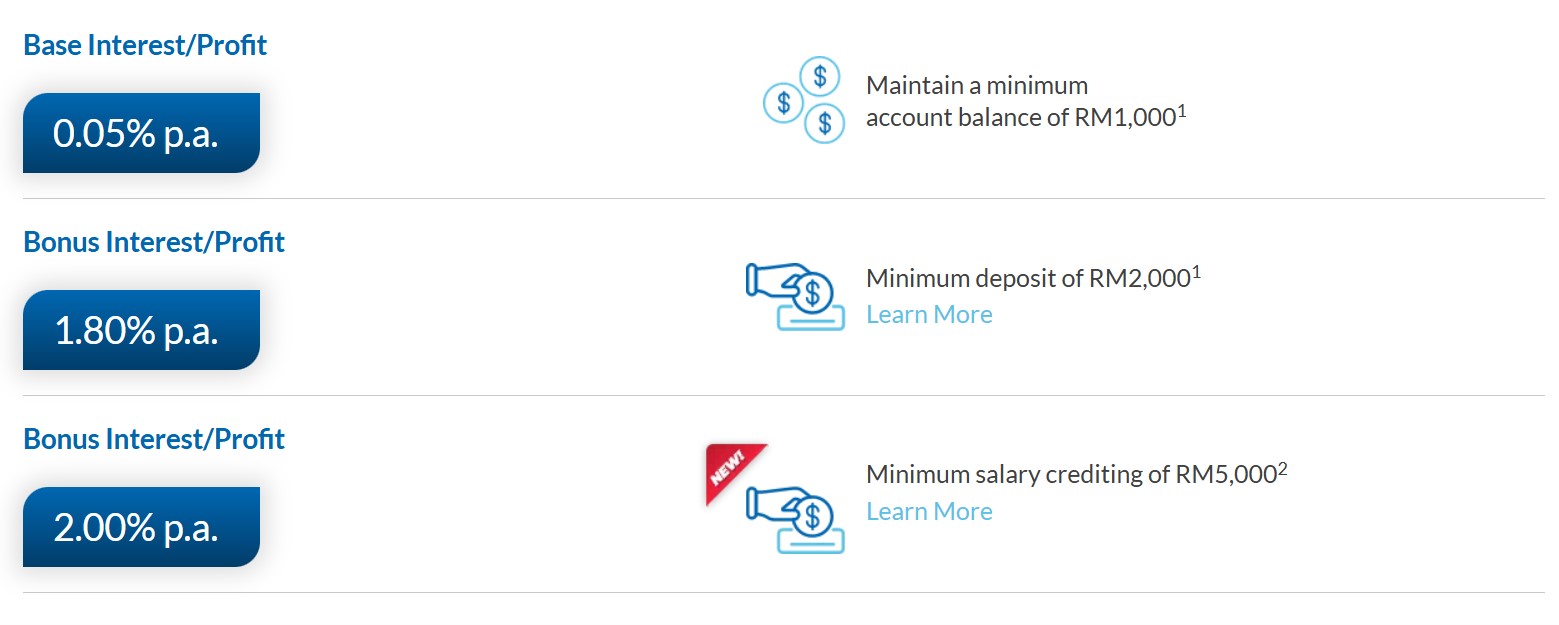

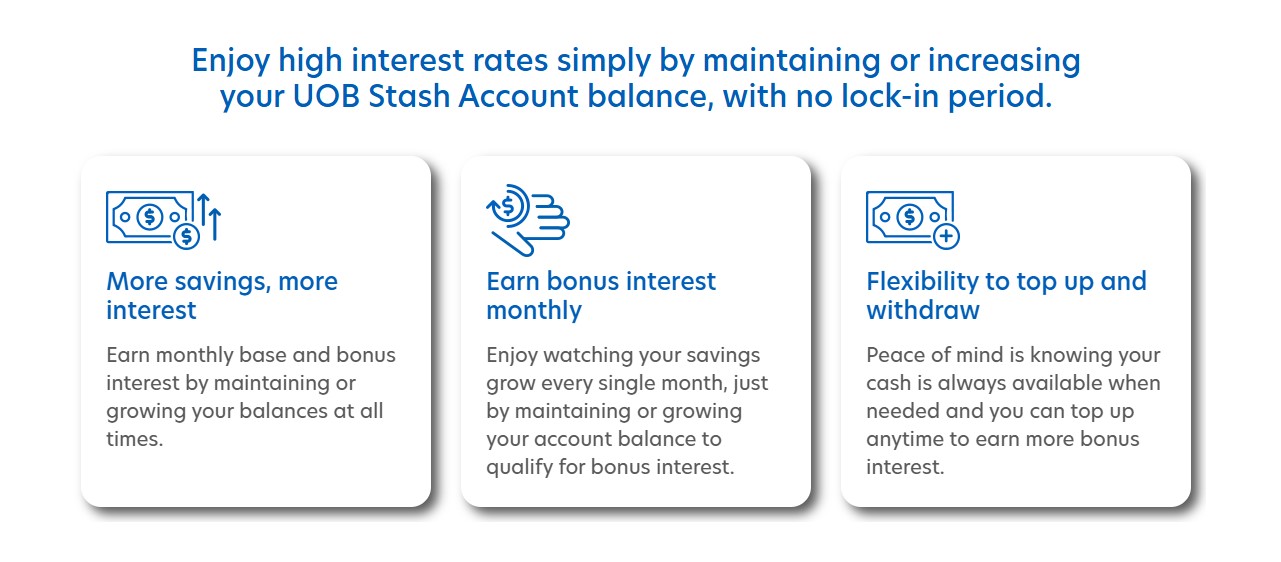

- 4. UOB Stash Account

- 5. Alliance SavePlus Account

- 6. OCBC 360 Account

- 7. Hong Leong Pay & Save Account

- 8. MBSB Rize Savings Account-i

- 9. MBSB Cash Rich Savings Account-i

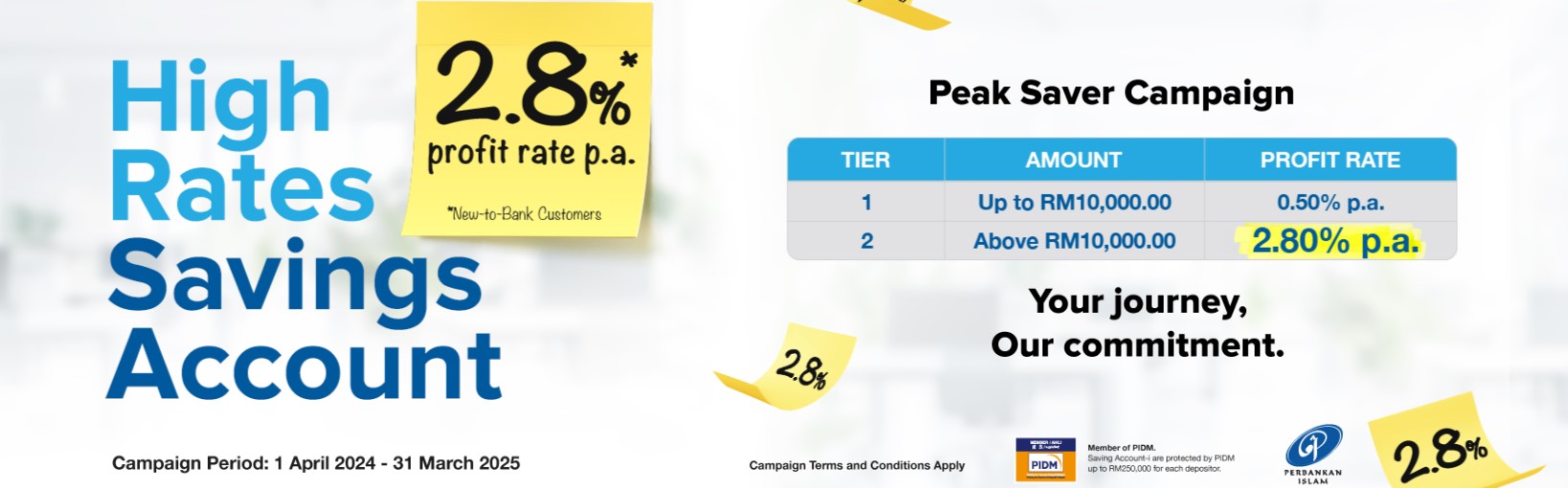

- 10. Affin Invikta Account

- The Digital-Bank Disruption: GX, Boost, AEON & Ryt

- How to Choose: A 4-Step Framework

- Worked Example: RM30,000 Over 12 Months

- Factors to Consider When Choosing a Savings Account

- Common Pitfalls to Avoid

- Frequently Asked Questions

- Conclusion

If you’re also weighing safer places to park cash, see our guides on Malaysia’s Best Fixed Deposit Rates and Best Low Risk Investments in Malaysia.

Quick Answer: Best Savings Account by Saver Type (2026)

| If you are… | Best pick | Indicative rate (p.a.) | Why |

|---|---|---|---|

| A hands-off saver who hates conditions | Boost Bank Savings | 3.30% daily, no conditions | Highest unconditional daily rate; withdraw anytime |

| Saving RM5k–RM50k and want flexibility | GX Bank + Bonus Pocket | 2.00% base / 3.18%–3.55% locked | Daily interest, keep base rate even if you withdraw |

| Happy to tap your card a few times a month | Ryt Bank | Up to 4.00% | Collect 5 “stamps” (RM10 transactions) to unlock |

| Want a Shariah-compliant digital option | AEON Bank Savings Pot | 3.00% | IFSA-licensed Islamic digital bank, PIDM-protected |

| Can credit salary + spend on a card | RHB Smart / SC Privilege$aver / UOB One | Up to 5.65%–6.60% | Highest headline rates if you meet every condition |

| Sitting on a large balance (RM200k+) | Alliance SavePlus / Affin Invikta | ~2.50%–2.75% | Tiered rates that reward big balances, few conditions |

Rates verified June 2026 from issuer and comparison sources; “up to” figures require meeting all monthly conditions. Confirm current rates with the bank before applying.

Full Comparison Table (June 2026)

| Account | Max rate (p.a.) | Min balance | Conditions to hit max | Type |

|---|---|---|---|---|

| RHB Smart Account/-i | Up to 6.60% | RM2,000 | Save + spend + invest tiers | Conventional/Islamic |

| Standard Chartered Privilege$aver | Up to 6.30% | None | Deposit, card spend, invest (valid to 31 Jan 2027) | Conventional |

| UOB One Account | Up to 5.65% | None | RM2,000 salary/transfer or RM500 card spend | Conventional |

| Ryt Bank | Up to 4.00% | None | 5 stamps/month (RM10 card or JomPAY each) | Digital |

| MBSB Rize Savings Account-i | Up to 4.00% | None | Campaign rate, any amount (confirm validity) | Islamic digital |

| Hong Leong Pay&Save | Up to 3.50% | RM10,000 | Deposit + bill pay + debit spend | Conventional |

| Boost Bank Savings | 3.30% (4.00% BoostUP Jar) | None | No conditions (Jar capped RM3,000 to 17 Nov 2026) | Digital |

| UOB Stash Account | Up to 3.20% | None | Grow/maintain monthly balance | Conventional |

| OCBC 360 Account/-i | Up to 3.00% (3.25% -i) | RM500 | Deposit + bills + card spend (rates cut May 2026) | Conventional/Islamic |

| AEON Bank Savings Pot | 3.00% | None | No conditions | Islamic digital |

| GX Bank (Bonus Pocket) | 2.00% base / up to 3.55% | None | Lock 3–6 months for higher tier | Digital |

| Alliance SavePlus | Up to ~2.75% | Tiered (high) | Large balance (RM500k+) | Conventional |

| Affin Invikta | Up to ~2.50% | RM250,000 | Large balance tier | Conventional |

1. UOB One Account

- Interest Rate: Up to 5.65% p.a. (on balances up to RM200,000)

- Minimum Balance: None

- Key Features:

- Earn the top tier by crediting RM2,000 salary, making a RM2,000 DuitNow/Interbank GIRO transfer, OR spending a combined RM500 on eligible UOB debit/credit cards each month.

- Tiered structure rewards higher balances; a RM250,000 deposit yields a blended effective rate of around 3.24% p.a.

- No minimum balance to open; track everything in the UOB TMRW app.

- Best For: Savers who reliably credit salary or spend on a UOB card every month.

2. Standard Chartered Privilege$aver

- Interest Rate: Up to 6.30% p.a. (on balances up to RM100,000; promotional rate valid to 31 January 2027)

- Minimum Balance: None for base interest

- Key Features:

- Bonus interest stacks for depositing funds, spending on a Standard Chartered credit card, and investing through the bank.

- One of the highest advertised rates in the market in 2026 — but you must hit all conditions to reach 6.30%.

- Comes with Priority/Privilege banking perks and investment advisory access.

- Best For: Customers who can meet multiple monthly conditions and want a premium banking relationship.

3. RHB Smart Account/-i

- Interest Rate: Up to 6.60% p.a. (on balances up to RM100,000)

- Minimum Balance: RM2,000

- Key Features:

- Rewards three behaviours — saving, spending and investing — each unlocking a slice of the bonus rate.

- Available in both conventional and Islamic (-i) versions.

- Manage everything through the RHB Mobile Banking app.

- Best For: Active RHB customers who bank, spend and invest under one roof.

4. UOB Stash Account

- Interest Rate: Up to 3.20% p.a. (confirm current tier with UOB)

- Minimum Balance: None

- Key Features:

- Pays bonus interest when your monthly balance is maintained or grows versus the previous month.

- Highest tiers apply to larger balances (typically RM100,000–RM200,000).

- No salary-crediting or card-spend conditions — simpler than the UOB One Account.

- Best For: Disciplined savers who keep adding to their balance and dislike spending conditions.

5. Alliance SavePlus Account

- Interest Rate: Up to ~2.75% p.a. (tiered; ~2.60% for RM200,001–RM500,000, ~2.75% above RM500,000)

- Minimum Balance: Best rates need a high balance

- Key Features:

- Simple tiered structure — the bigger your balance, the better the rate — with no spend or salary conditions.

- No complex hoops or hidden fees; monthly e-statements.

- Also available as a Shariah-compliant SavePlus Account-i.

- Best For: High-balance savers wanting a low-maintenance home for idle cash.

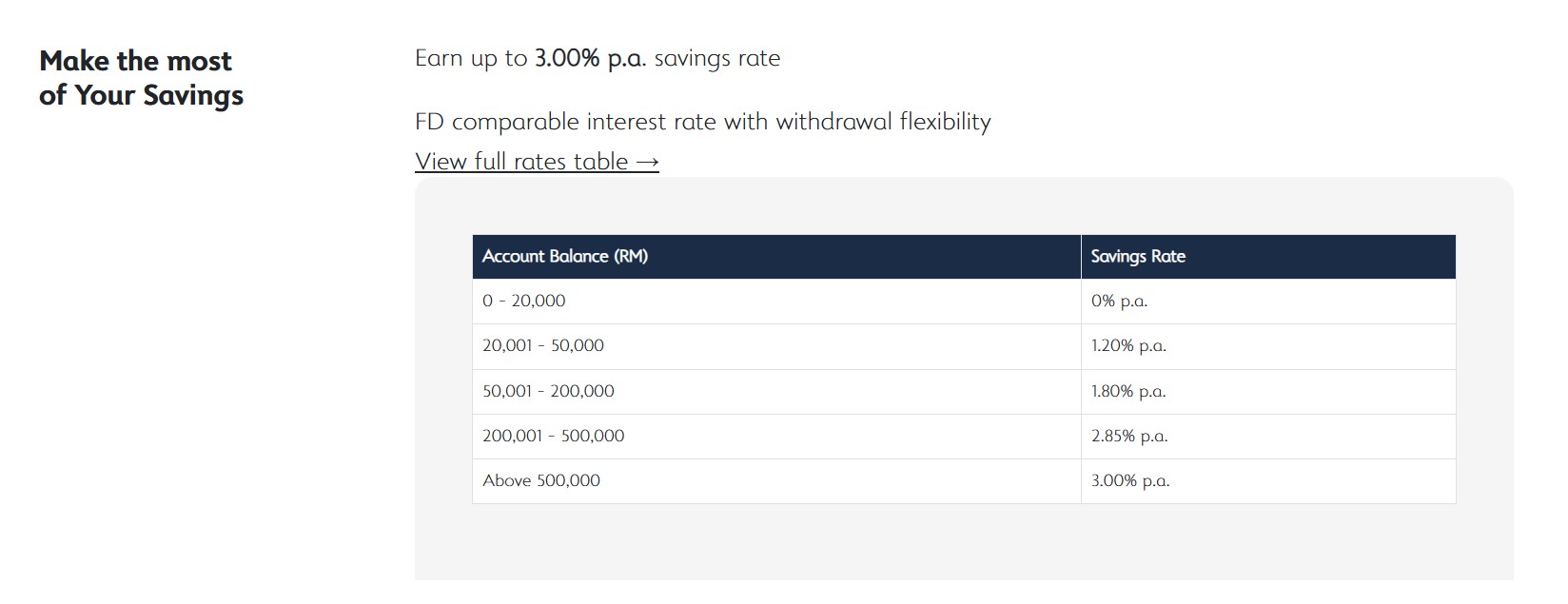

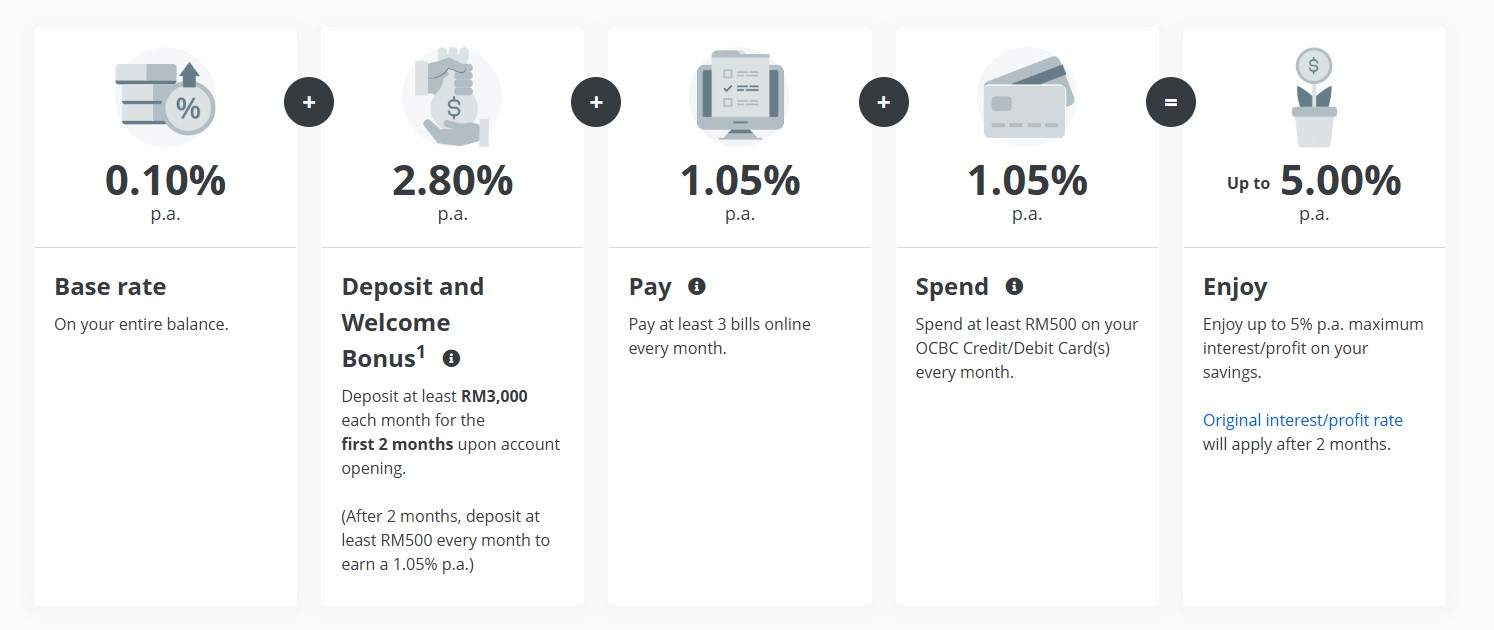

6. OCBC 360 Account

- Interest Rate: Up to 3.00% p.a. (conventional) / up to 3.25% p.a. (360 Account-i) on the first RM100,000 — note OCBC trimmed bonus rates from May 2026

- Minimum Balance: RM500

- Key Features:

- Stack bonus interest by depositing at least RM500, paying 3 bills online, and spending RM500 on an OCBC card each month.

- New customers can earn up to 5.00% p.a. for the first 2 months as a sign-up boost.

- Base interest of just 0.10% p.a. applies if you skip the conditions — so this account only pays off if you actively use it.

- Best For: Salaried users who can comfortably meet all three monthly conditions.

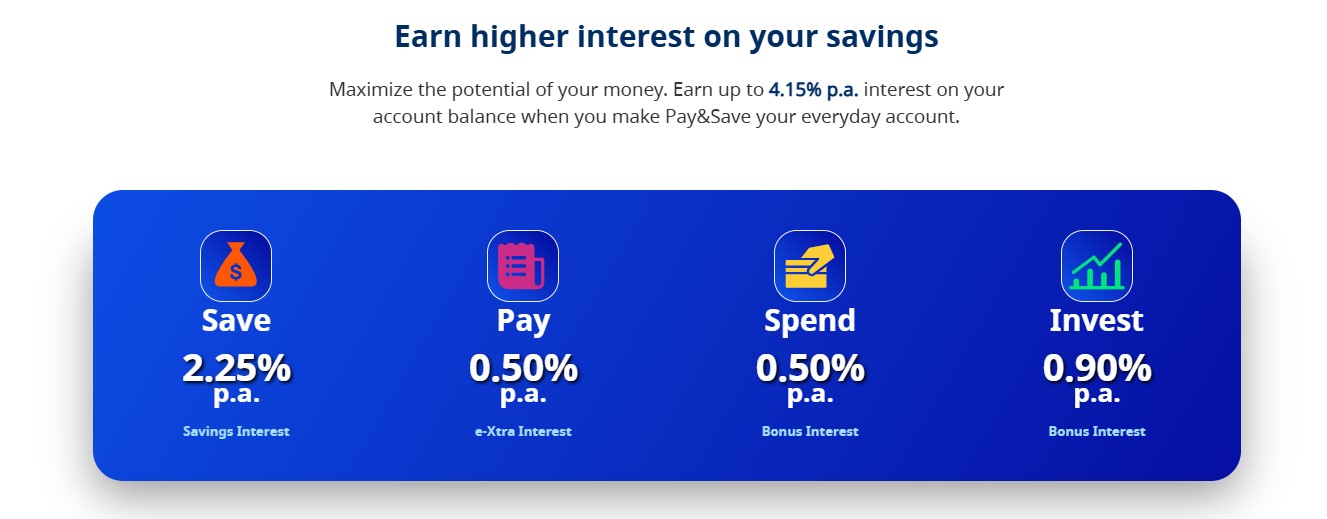

7. Hong Leong Pay & Save Account

- Interest Rate: Up to 3.50% p.a. (on balances up to RM100,000)

- Minimum Balance: RM10,000 to unlock bonus tiers

- Key Features:

- Bonus interest for meeting actions like monthly deposits and debit-card spending.

- Free financial-planning tools and alerts via Hong Leong Connect.

- Flexible access with no withdrawal penalties.

- Best For: Active users comfortable transacting monthly to maximise interest.

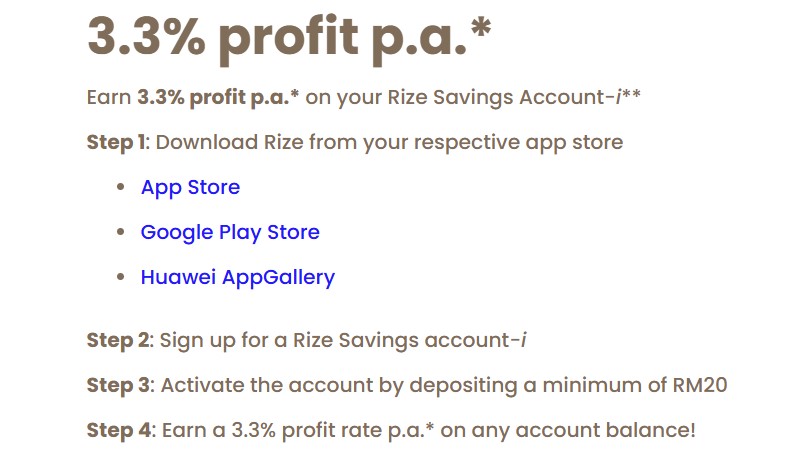

8. MBSB Rize Savings Account-i

- Interest Rate: Up to 4.00% p.a. (special deposit campaign — any amount, no tiers; confirm current validity)

- Minimum Balance: None

- Key Features:

- Shariah-compliant account on MBSB’s Rize app with competitive promotional profit rates.

- Fully online opening with minimal documentation.

- Campaign rates can change, so check the in-app terms before locking in funds.

- Best For: Savers wanting a high promotional Islamic rate with online convenience.

9. MBSB Cash Rich Savings Account-i

- Interest Rate: Tiered profit rate (confirm current rate with MBSB; standard tier is modest versus the Rize campaign above)

- Minimum Balance: None

- Key Features:

- Shariah-compliant option for Islamic-banking users who prefer a branch-backed account.

- No minimum balance requirement.

- PIDM-protected up to RM250,000 per depositor.

- Best For: Conservative Islamic savers who want simplicity over chasing promo rates.

10. Affin Invikta Account

- Interest Rate: Up to ~2.50% p.a. (top tier needs a balance of roughly RM250,000–RM4 million)

- Minimum Balance: Varies by tier

- Key Features:

- Tiered rates reward larger balances, with preferential rates on linked loans and investments.

- Accessible through both online and branch banking.

- Aimed at affluent savers rather than everyday accounts.

- Best For: High-net-worth savers who keep large idle balances.

The Digital-Bank Disruption: GX, Boost, AEON & Ryt

The single biggest change since 2024 is that Malaysia’s BNM-licensed digital banks now pay strong rates with far fewer strings than the conditional accounts above. Crucially, all of them are genuine bank deposits covered by PIDM up to RM250,000 — not investments.

- Ryt Bank — up to 4.00% p.a., unlocked by collecting 5 “stamps” a month (each stamp = a RM10+ transaction via the Ryt Card or JomPAY).

- Boost Bank — 3.30% p.a. credited daily with zero conditions, the highest unconditional daily rate in 2026. Its promotional BoostUP Jar pays 4.00% p.a. (daily-compounding) but is capped at RM3,000 and runs until 17 November 2026.

- AEON Bank Savings Pot — 3.00% p.a., Shariah-compliant and IFSA-licensed; ideal if you want a no-conditions Islamic option.

- GX Bank — 2.00% p.a. base, credited daily; its Bonus Pocket pays 3.18% p.a. (3-month lock) or 3.55% p.a. (6-month lock), and you keep the 2.00% base even if you withdraw early.

For most Malaysians with an emergency fund of RM5,000–RM50,000, a digital bank now beats a conditional 6% account that you can’t realistically max out. Pair one with a solid debit card and you have a fee-free everyday setup.

How to Choose: A 4-Step Framework

- Match the rate to your real balance. A 6.60% headline that only applies to the first RM100,000 — and only if you save, spend and invest — is worth nothing if you keep RM8,000 and never invest. Work out your effective rate, not the marketing rate.

- Count the conditions you’ll actually meet. If you can credit salary and spend on a card anyway, a conditional account is free money. If you can’t, a no-conditions digital bank (Boost, AEON, GX base) wins.

- Separate emergency cash from “growth” cash. Keep 3–6 months of expenses in an instant-access account (see our emergency fund guide); push surplus into a fixed deposit or low-risk investment for a higher locked return.

- Confirm PIDM coverage. Every account here is PIDM-insured to RM250,000 per depositor per bank. If you hold more, spread it across banks.

Worked Example: RM30,000 Over 12 Months

Say you have RM30,000 and can’t reliably meet salary + spend + invest conditions:

- Standard savings account (0.25%): ~RM75 interest/year.

- Boost Bank (3.30%, no conditions): ~RM990/year.

- Ryt Bank (4.00%, with 5 stamps/month): ~RM1,200/year.

- Conditional 6% account but you only meet half the tiers (~3%): ~RM900/year — often less than a no-conditions digital bank.

The lesson: the rate you can actually earn beats the rate on the poster.

Factors to Consider When Choosing a Savings Account

- Interest structure: Understand the tiers and exactly which actions unlock the top rate.

- Minimum balance: Match it to what you can realistically keep.

- Bonus conditions: Decide whether salary crediting, bill payments or card spend fit your habits.

- Fees: Watch for below-minimum-balance fees, early-closure charges and dormancy fees.

- Accessibility: App-only digital banks are convenient but have no branches — a factor for some.

- Shariah compliance: AEON Bank, RHB Smart-i, OCBC 360-i and MBSB Rize-i offer Islamic options.

Common Pitfalls to Avoid

- Chasing the headline rate you can’t qualify for, then earning the 0.10% base instead.

- Confusing “investment accounts” with savings — some high-yield products are not PIDM-protected. Always check.

- Ignoring promo expiry dates (e.g. SC Privilege$aver to 31 Jan 2027, Boost Jar to 17 Nov 2026) and finding your rate has dropped.

- Leaving your full emergency fund in a capped Jar (e.g. Boost’s 4% caps at RM3,000) — only the capped amount earns the top rate.

Frequently Asked Questions

Conclusion

Malaysia’s savings market in 2026 is the most competitive it has been in years. If you can meet monthly conditions, RHB Smart, SC Privilege$aver and UOB One offer the highest headline rates. If you want simplicity, the digital banks — Boost, Ryt, AEON and GX — now pay 3–4% with little effort and full PIDM protection. Match the account to your balance and habits, keep your emergency fund liquid, and always confirm the latest rate and conditions before opening an account.

Disclaimer: This guide is provided by KayaToday for general information only and is not financial advice. Rates and conditions were verified in June 2026 from issuer websites and reputable comparison sources (RinggitPlus, StashAway, iMoney), but high-interest savings rates change frequently and promotional rates expire. This list is not exhaustive — always confirm current rates, eligibility and terms directly with the bank before opening an account.

Outbound references: Bank Negara Malaysia – OPR Decisions · PIDM deposit insurance · RinggitPlus savings comparison.

![Malaysia Best Fixed Deposit Rates [July 2026]](https://kayatoday.com/wp-content/uploads/2025/07/Best-Fixed-Deposit-Rate-Malaysia-300x170.jpg)