Calculate Your Loan Repayment Instantly

- Calculate Your Loan Repayment Instantly

- SME Loans in Malaysia 2026: Quick Answer

- What counts as an SME in Malaysia?

- Manufacturing sector

- Services & other sectors

- Why SME financing matters in 2026

- The real challenges SMEs face when borrowing

- Financing access and paperwork

- Cash flow and rising operating costs

- Digital transformation

- Eligibility criteria for SME business loans

- Business registration and ownership

- Financial standing and credit score

- Other common conditions

- Top SME loan providers in Malaysia (2026)

- How to choose the right SME loan

- Government schemes & where to apply for assistance (2026)

- Budget 2026 highlights for SMEs

- BNM Fund for SMEs facilities

- Micro & targeted schemes

- Development Financial Institutions (DFIs)

- When does an SME loan make sense? (Worked scenarios)

- Common pitfalls to avoid

- Frequently Asked Questions

Verified June 2026. Rates, scheme allocations and eligibility change frequently — always confirm the latest figures with the bank or agency before you apply.

SME Loans in Malaysia 2026: Quick Answer

If you only have a minute, here is the shortlist for 2026. Government-linked lenders give the cheapest money but take longer to approve; commercial banks are faster but want a track record; digital and peer-to-peer (P2P) platforms are fastest of all but cost the most.

| Best for… | Where to look | Indicative 2026 rate |

| Lowest overall rate | SME Bank, BNM Fund for SMEs facilities | From ~3.50% p.a. |

| Automation / digitalisation | BNM Automation & Digitalisation Facility (ADF) | Up to 4% p.a. (incl. guarantee fee) |

| Green / high-tech projects | BNM High Tech & Green Facility (HTG) | Up to 3.5% (no guarantee) / 5% (incl. guarantee) |

| Established business, bigger limit | Maybank, CIMB, RHB, HSBC, Alliance SME loans | From ~4.50% p.a. |

| Micro business / first loan | TEKUN, BSN BizMula, CGC BizWanita | From ~4% flat p.a. |

| Fastest cash (no collateral) | P2P platforms (Funding Societies, microLEAP), Boost Capital | ~0.8%–1.5% per month |

The rest of this guide explains who qualifies, what each option really costs, the 2026 government schemes worth knowing, and how to choose between them. For background reading, see our guides to the best personal loans in Malaysia and how to check your CTOS credit score before you apply.

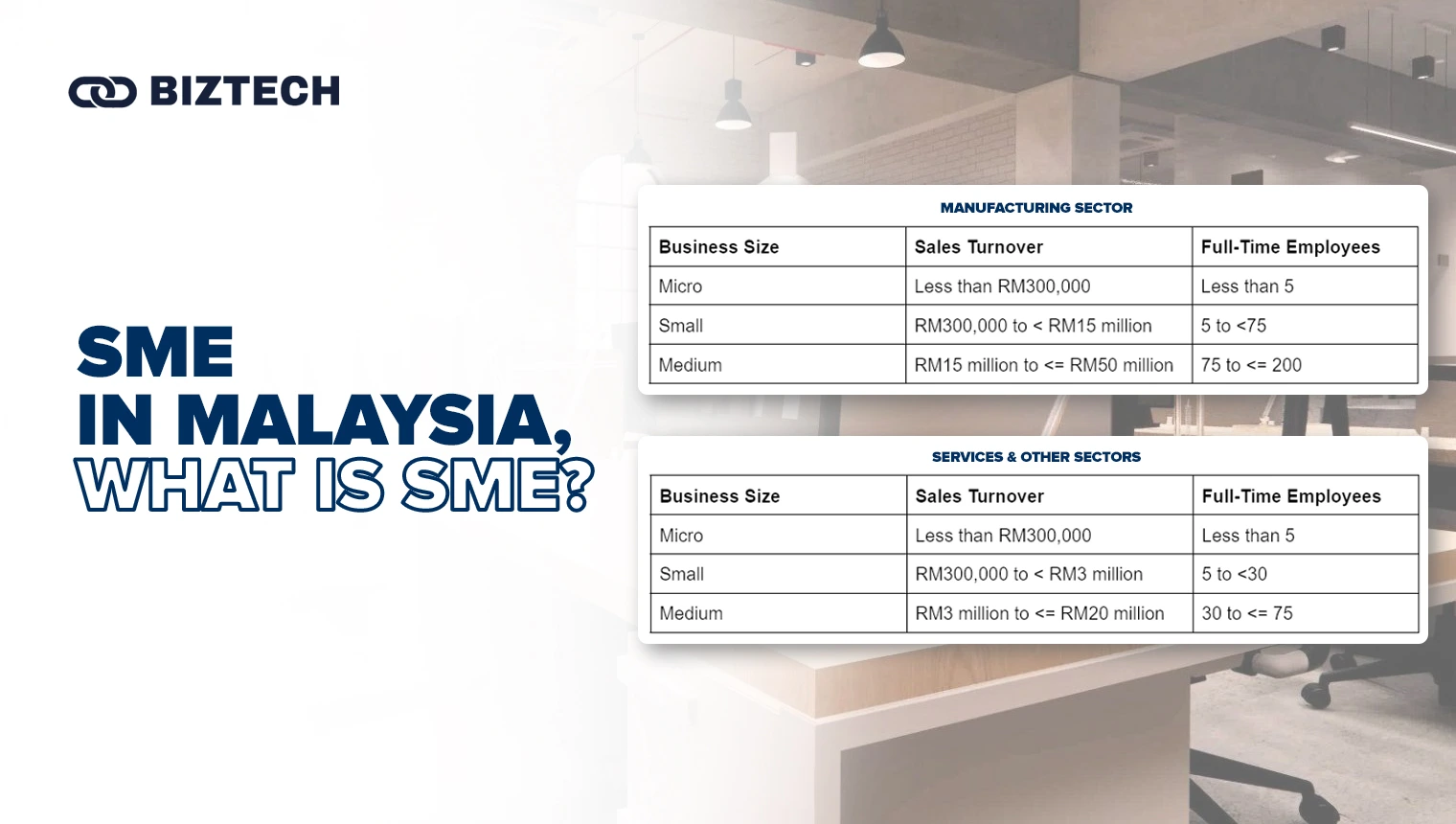

What counts as an SME in Malaysia?

Small and medium-sized enterprises (SMEs) are the backbone of Malaysia’s economy. Whether you qualify for an SME loan, a government scheme or a grant usually starts with one question: does your business fit the official SME definition coordinated by SME Corp. Malaysia? That definition has not changed for 2026 and is based on either annual sales turnover or number of full-time employees — whichever puts you in the lower category.

Manufacturing sector

| Business Size | Sales Turnover | Full-Time Employees |

| Micro | Less than RM300,000 | Less than 5 |

| Small | RM300,000 to < RM15 million | 5 to < 75 |

| Medium | RM15 million to ≤ RM50 million | 75 to ≤ 200 |

Services & other sectors

| Business Size | Sales Turnover | Full-Time Employees |

| Micro | Less than RM300,000 | Less than 5 |

| Small | RM300,000 to < RM3 million | 5 to < 30 |

| Medium | RM3 million to ≤ RM20 million | 30 to ≤ 75 |

A few rules that trip people up: a “full-time employee” means someone paid for at least six hours a day and 20 days a month (or 120 hours a month). You only need to satisfy one of the two criteria, and classification uses whichever is lower. If you exceed both thresholds for two consecutive financial years you stop being an SME; the reverse is also true. Your business must be registered with the Companies Commission of Malaysia (SSM). Public-listed companies on the main board and their subsidiaries, multinationals, government-linked companies and state-owned enterprises are excluded.

Why SME financing matters in 2026

SMEs make up roughly 97% of all business establishments in Malaysia and contribute close to 40% of national GDP (figures vary slightly by reporting year — confirm the latest in SME Corp’s annual report). The overwhelming majority are microenterprises, with the balance split between small and medium firms. They drive employment, innovation and competition.

Their biggest single constraint remains access to financing. That is exactly why Bank Negara Malaysia (BNM) and the government keep topping up dedicated SME funds — the BNM Fund for SMEs now stands at around RM34.9 billion after a further RM2.5 billion was added with a focus on first-time borrowers. With the Overnight Policy Rate (OPR) held at 2.75% (where it has sat since July 2025 and through the May 2026 meeting), borrowing costs in 2026 are relatively stable rather than rising. That makes it a reasonable window to lock in financing — provided the loan genuinely earns its keep.

The real challenges SMEs face when borrowing

Knowing the obstacles upfront helps you prepare a stronger application.

Financing access and paperwork

Banks apply strict checks: most commercial lenders want two years of audited accounts, six months of business bank statements, SSM documents and either collateral or a government guarantee. Micro and newer businesses often can’t meet that bar — which is precisely the gap that government schemes and P2P platforms exist to fill.

Cash flow and rising operating costs

Many micro-SMEs run on thin margins and get squeezed when input, fuel or electricity costs rise. Working-capital and invoice financing are designed for this timing mismatch — bridging the gap between paying suppliers and getting paid by customers — rather than for long-term expansion.

Digital transformation

Adopting automation, e-invoicing and data tools costs money upfront. The good news is that BNM’s Automation & Digitalisation Facility and High Tech & Green Facility are purpose-built (and subsidised) for exactly these investments — so a digitalisation project can often be financed more cheaply than a general-purpose loan.

Eligibility criteria for SME business loans

Requirements differ by lender, but most assess these core areas.

Business registration and ownership

Your business must be SSM-registered (sole proprietorship, partnership or private limited company). Most banks require the company to be at least 51% Malaysian-owned, and many ask for a minimum operating history — commonly two years for commercial banks, though some online and P2P lenders accept just one year (and a few government micro-schemes accept newer businesses).

Financial standing and credit score

Over 90% of SME financing in Malaysia comes from banks and financial institutions, so lenders scrutinise your creditworthiness, repayment capacity and history. Both the business and its directors are checked against CCRIS and CTOS records. A clean record improves your odds and your rate — it is worth pulling your report first (here’s how to check and improve your CTOS score) and clearing any director-level personal arrears before applying.

Other common conditions

Lenders often set an age range for the principal owner (for example 25–65), a minimum annual turnover, and sector or purpose restrictions for subsidised schemes. There is also a stamp-duty exemption on loan agreements for credit facilities approved under BNM-funded schemes. Always read the full terms — fees and early-settlement rules vary widely.

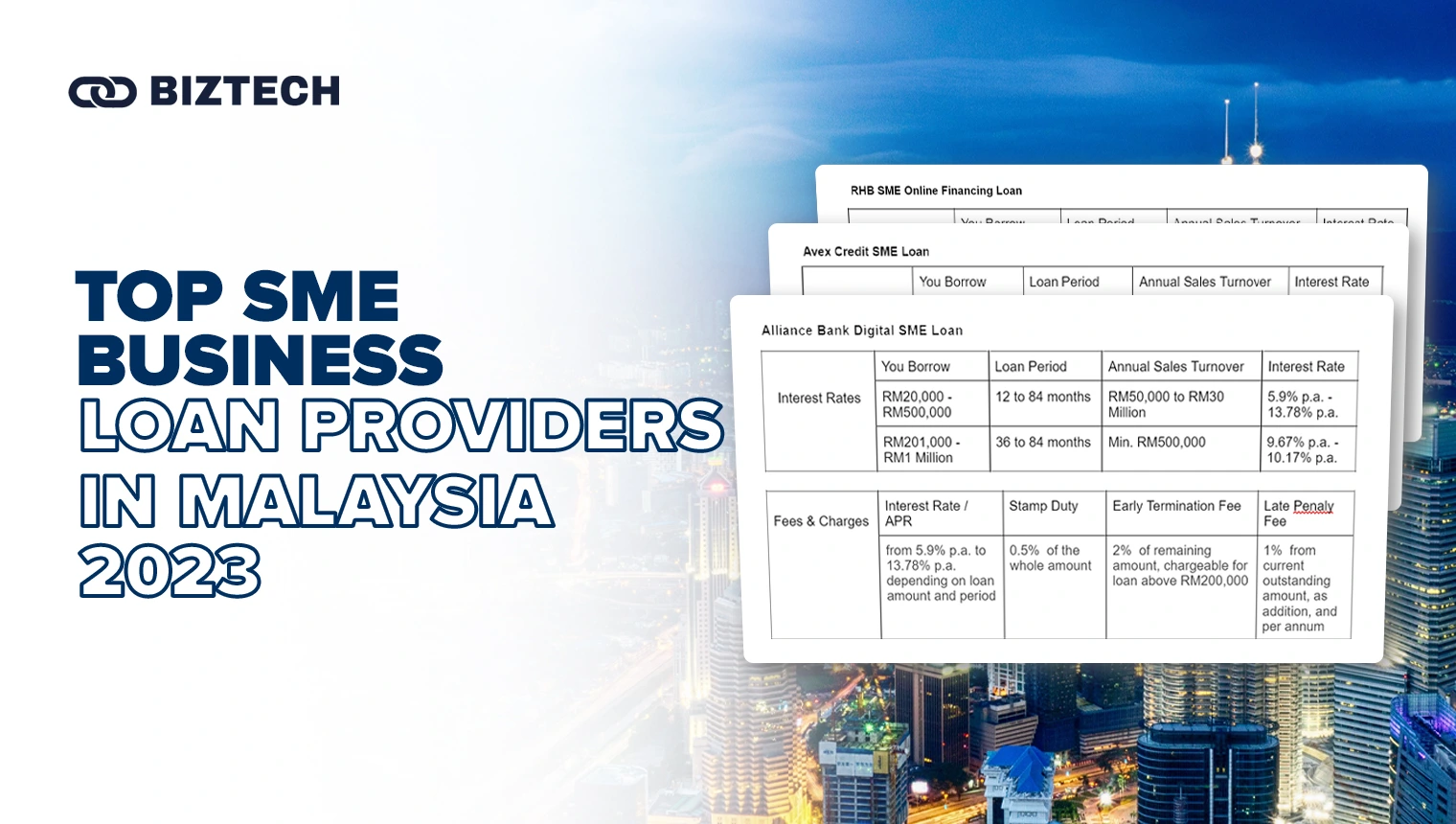

Top SME loan providers in Malaysia (2026)

Below are widely used commercial and digital lenders. Rates shown are the lenders’ published or indicative figures and move with each campaign — treat them as a starting point and confirm the current rate, fees and tenure directly with the provider before applying.

| Provider | Loan Amount | Tenure | Indicative Rate (p.a.) | Best for |

| SME Bank (BAP RMK-12) | RM50,000 – RM1 million | Up to 7 years (+ up to 12-mth grace) | ~4% flat | Lowest cost, longer tenure |

| Maybank SME Digital Financing | RM10,000 – RM250,000 | Up to 60 months | From ~4.50% | Fast online, existing Maybank SMEs |

| RHB SME Online Financing | ~RM50,000 – RM1 million | 6 to 84 months | From ~8.45% | Quick approval, 1-yr min history |

| Alliance Bank Digital SME Loan | RM20,000 – RM1 million | 12 to 84 months | ~5.90% – 13.78% | Flexible tenure, “Support Lokal” |

| HSBC Working Capital Term Loan | RM100,000 – RM500,000 | 12 to 60 months | From ~9.89% | No lock-in, high financing margin |

| Capital by Boost (Boost Credit) | RM1,000 – RM100,000 | Up to 12 months | ~18% (Wakalah fee ~RM50) | Fast cash, no guarantor |

| Funding Societies / microLEAP (P2P) | From RM1,000 (up to ~RM500,000) | 1 to 18 months | ~0.8% – 1.5% per month | Working capital, invoice financing |

Common fees to watch: stamp duty (0.5% of the loan, often exempt under BNM-funded schemes), early-settlement fees (RHB and HSBC often charge none; some others charge 2% of the outstanding amount or several months’ interest), and late-payment penalties (typically ~1% p.a. of the outstanding amount, but as high as 8% with some non-bank lenders). A “low” headline rate with a stiff early-settlement penalty can cost more than a slightly higher rate with no lock-in.

If you want to model monthly repayments before you commit, our loan calculator guide explains how flat rates convert to an effective rate (the effective rate is usually roughly 1.8–2× the flat rate).

How to choose the right SME loan

- Match the loan to the purpose. Short-term cash-flow gap → working capital or invoice financing. Equipment or expansion → a term loan over a longer tenure. Digitalisation or green upgrade → a BNM subsidised facility.

- Compare the effective rate, not the flat rate. Always ask for the effective (reducing-balance) rate so you compare like with like.

- Check eligibility before applying. Each rejected application can leave a footprint — confirm you meet the turnover, age and operating-history rules first.

- Prioritise flexibility. No lock-in and no early-settlement fee give you room to refinance if a cheaper scheme opens up.

- Exhaust the cheap money first. Government and BNM-funded schemes are almost always cheaper than commercial or P2P options — start there if you qualify and can wait for approval.

Government schemes & where to apply for assistance (2026)

Beyond commercial banks, a large slice of SME funding flows through government agencies, development financial institutions (DFIs) and BNM’s dedicated funds. Budget 2026 is notably SME-heavy.

Budget 2026 highlights for SMEs

Budget 2026 channels around RM50 billion towards business financing overall, including roughly RM40 billion of funds, guarantees and grants aimed at SMEs. Highlights include about RM20 billion in loan guarantees through Syarikat Jaminan Pembiayaan Perniagaan (SJPP) — of which RM5 billion is ring-fenced for Bumiputera SMEs — and RM2.5 billion for micro-loans via TEKUN Nasional and Bank Simpanan Nasional (BSN). A new Government Guarantee Scheme MADANI 2026 (GGSM4) covers both working capital and capital expenditure.

BNM Fund for SMEs facilities

These are among the cheapest financing options available, channelled through participating banks:

| Facility | Purpose | Indicative Rate |

| High Tech & Green Facility (HTG) | High-tech, innovation, green & low-carbon projects | Up to 3.5% (no guarantee) / 5% incl. guarantee fee |

| Automation & Digitalisation Facility (ADF) | Equipment, automation, software, digitalisation | Up to 4% p.a. incl. guarantee fee |

| Disaster Relief Facility (DRF) | Recovery after floods / disasters | Up to 3.5% p.a. incl. guarantee fee |

Micro & targeted schemes

TEKUN Nasional offers micro-loans up to RM100,000 at a 4% flat rate with tenures up to 10 years. BSN BizMula supports businesses operating for less than four years, while CGC BizWanita is a guarantee scheme for women-owned SMEs that lack full collateral. SME Bank’s Business Accelerator Programme (BAP RMK-12) provides RM50,000–RM1 million at around 4% flat for up to seven years.

Development Financial Institutions (DFIs)

DFIs such as SME Bank, Bank Rakyat, Agrobank and BSN are set up to fund specific sectors and offer loans, equity and advisory support. They typically carry the lowest rates but require more documentation and take longer to approve than a commercial bank’s online product.

When does an SME loan make sense? (Worked scenarios)

Borrowing to grow can be smart; borrowing to plug a structural loss usually is not. Three realistic examples:

Scenario 1 — Bridging a big order. Lina’s home-baking side hustle outgrows her kitchen. A short Capital by Boost facility (fast, no guarantor) lets her lease a small shoplot in Klang Valley and buy ovens. Because the loan funds revenue-generating capacity that more than covers the ~18% cost, it pays for itself.

Scenario 2 — Starting up with a cheaper scheme. Fresh graduate David launches a retail business with a partner. Rather than an expensive commercial loan, he applies to SME Bank’s Business Accelerator Programme — up to RM1 million at ~4% flat over seven years — trading slower approval for a far lower cost of funds.

Scenario 3 — Fulfilling a supply contract. Visber’s vegetable farm wins a supermarket supply deal it can’t currently fill. An HSBC Working Capital Term Loan funds the expansion; the recurring contract revenue services the repayment comfortably.

The common thread: each loan funds something that generates more cash than it costs. Before signing, run the numbers — if the financing cost eats your margin, restructure the deal or wait.

Common pitfalls to avoid

Comparing flat rates against effective rates and assuming they’re equal; ignoring early-settlement penalties that lock you into a pricey loan; borrowing for working capital on a long tenure (you pay interest for years on a short-term gap); overlooking cheaper BNM-funded or government schemes because the paperwork looks daunting; and applying to many lenders at once, which can dent your credit profile. If cash flow is already strained, talk to AKPK before taking on more debt.

Frequently Asked Questions

Disclaimer: This guide is provided by KayaToday for general information only and is not financial advice. Interest rates, fees, scheme allocations and eligibility criteria are accurate to the best of our knowledge as of June 2026 but change frequently. Always verify the latest terms directly with the bank, agency or BNM before making any borrowing decision.