Ever wondered what lenders actually see when you apply for a loan or credit card in Malaysia? Much of it comes down to your CTOS Report and the three-digit CTOS Score inside it. That score helps decide whether your home loan, car loan or credit card gets approved — and often what interest rate you’re offered. The good news: you can check it yourself, and you can move it in the right direction with a few consistent habits.

- CTOS vs CCRIS: Quick Answer

- Checking Your CTOS Score

- Step-by-Step Guide to Checking Your Score Online

- Using the CTOS / MyCTOS Smartphone App

- Checking Your Free CCRIS Report (Bank Negara)

- Understanding Your CTOS Score

- How Is Your CTOS Score Calculated?

- What Is a Good CTOS Score?

- Improving Your CTOS Score

- 1. Pay Every Bill on Time

- 2. Manage Your Credit Utilisation

- 3. Be Strategic About New Applications

- 4. Review and Dispute Errors

- Overcoming Common CTOS Challenges

- What to Do After a Loan Rejection

- Recovering From a Default or AKPK Status

- Frequently Asked Questions

- Conclusion

This guide explains how to check your CTOS Score (and your free CCRIS report from Bank Negara), how the score is actually calculated in 2026, what counts as a “good” score, and the practical steps that genuinely improve it. Figures and processes verified June 2026 — always confirm the latest details on CTOS and Bank Negara’s official sites, as pricing and access methods change.

CTOS vs CCRIS: Quick Answer

A common mix-up: CCRIS and CTOS are not the same thing. CCRIS is the raw lending database run by Bank Negara Malaysia; CTOS is a private credit reporting agency that pulls in CCRIS data plus other public records and turns it into a single score. Here’s how the main ways to check your credit stack up:

| Report | Who provides it | Shows a score? | Cost (2026) | Best for |

|---|---|---|---|---|

| CCRIS report | Bank Negara Malaysia (eCCRIS) | No — raw loan & repayment data only | Free | Seeing exactly what banks report about your loans |

| MyCTOS Basic Report | CTOS | Limited | Free (limited access) | A quick look at your CTOS profile & records |

| MyCTOS Score Report | CTOS | Yes — full CTOS Score (300–850) + CCRIS | ~RM26.50–RM27.90 | The complete picture before a big loan application |

| CTOS SecureID | CTOS | Yes — with monitoring & alerts | ~RM99/year | Ongoing credit monitoring & fraud alerts |

Bottom line: if you only want to know what banks see, your CCRIS report from Bank Negara is free. If you want the actual CTOS Score number that many lenders glance at first, you’ll usually need the paid MyCTOS Score Report.

Checking Your CTOS Score

Understanding your CTOS Score is the first step to managing it. Here are the main ways to access your report and score.

Step-by-Step Guide to Checking Your Score Online

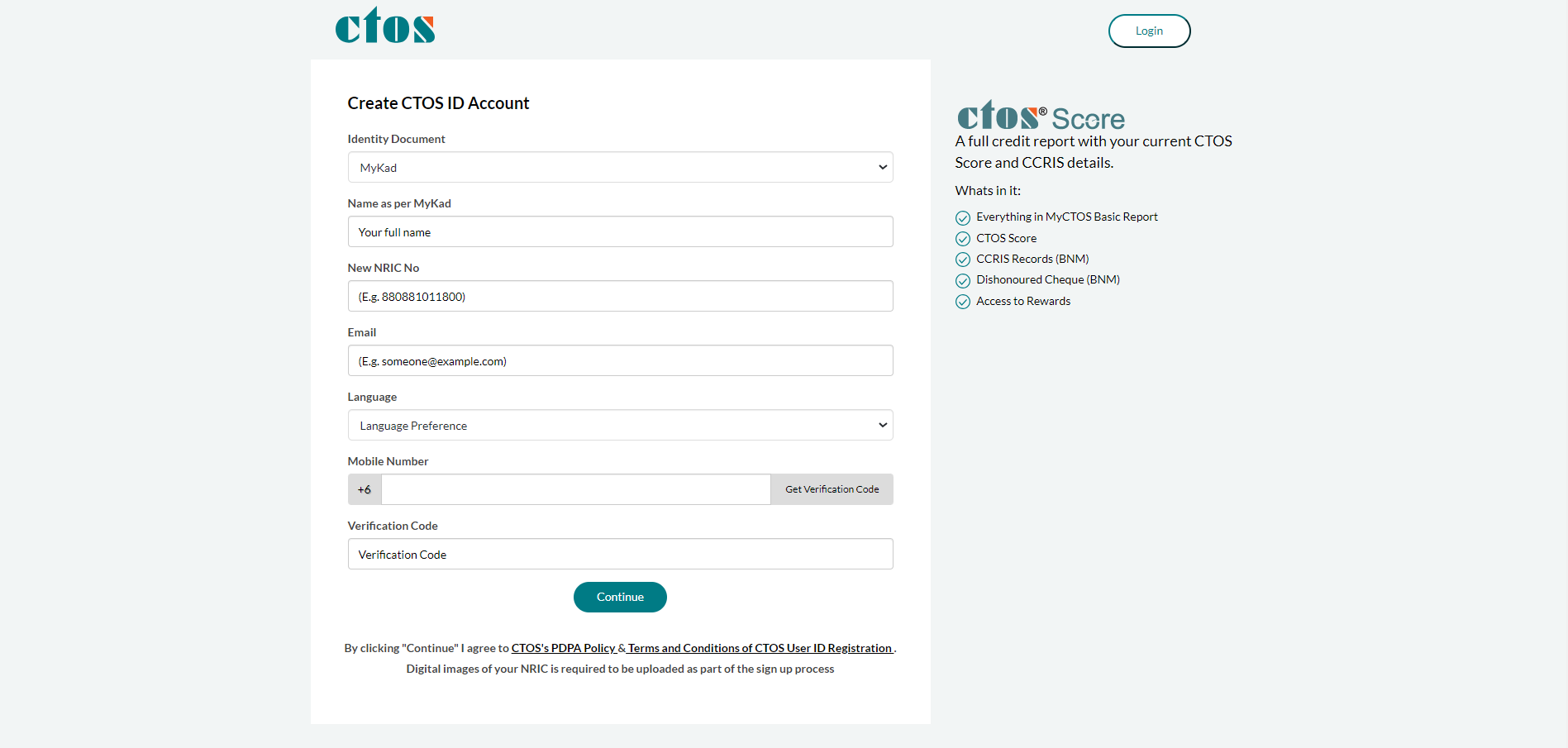

1. Head over to the official CTOS website: ctoscredit.com.my

2. Register for a MyCTOS account: Provide your NRIC/MyKad (or passport) number and the requested details. You’ll verify your identity electronically — CTOS now uses e-KYC (a MyKad scan plus a selfie/facial check) so you can register without visiting a branch.

3. Activate your account: Verify your email address and complete the activation process.

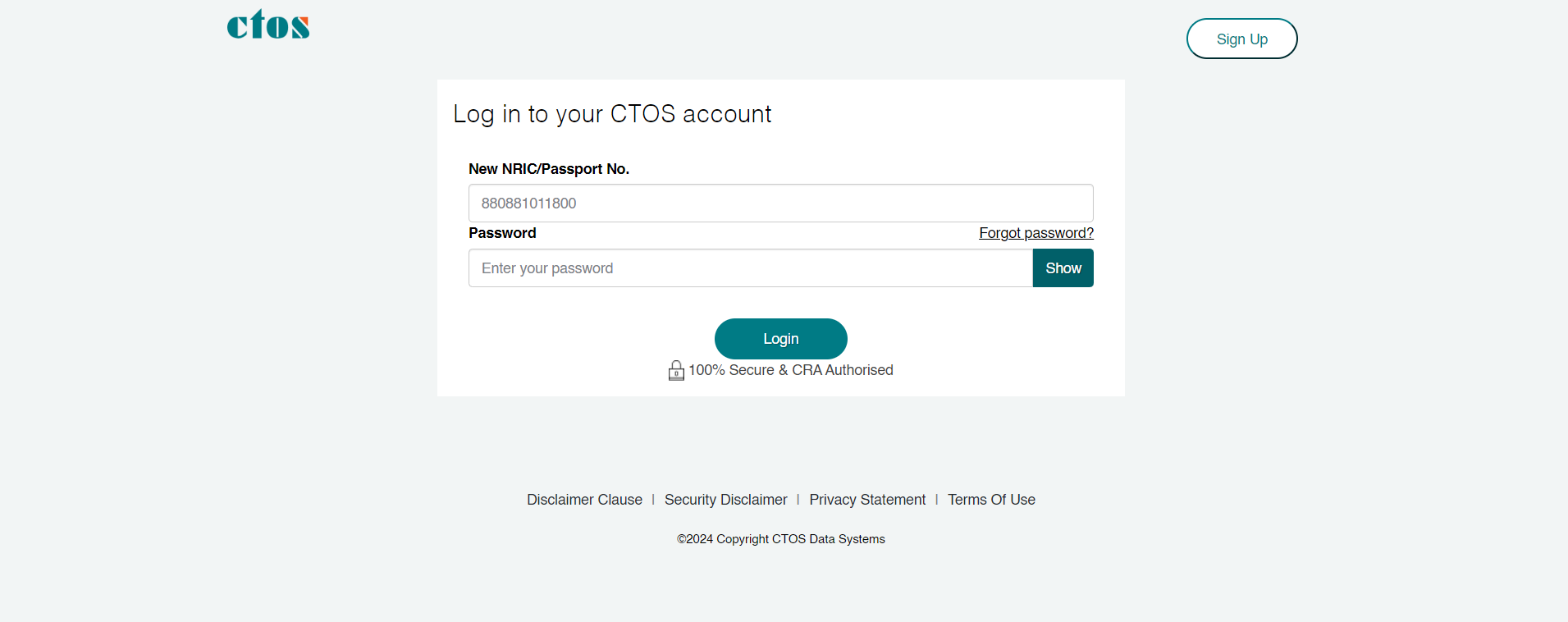

4. Log in and pull your report: Once activated, log in to MyCTOS. To see your actual CTOS Score and CCRIS records, purchase the MyCTOS Score Report (around RM26.50–RM27.90). The free MyCTOS Basic Report shows your CTOS profile but not the full score.

Using the CTOS / MyCTOS Smartphone App

1. Download the CTOS app from the App Store, Google Play or Huawei AppGallery.

2. Register or log in using your MyCTOS credentials.

3. The app displays your CTOS Score and gives you access to your report anytime — handy for tracking changes before you apply for financing.

Checking Your Free CCRIS Report (Bank Negara)

Many Malaysians don’t realise the underlying credit data is available free, straight from the source. Your CCRIS report — outstanding loans, 12 months of repayment conduct, pending applications and any Special Attention Accounts — can be checked at no cost:

- eCCRIS portal: Register at Bank Negara’s CCRIS service (eccris.bnm.gov.my), verify your identity, and view or download your report online — typically one free report per day.

- CCRIS kiosk: Visit a self-service kiosk at a BNM office or AKPK branch with your MyKad for an instant printout.

Reading CCRIS alongside your CTOS Score gives you the full story — the score tells you how you look to lenders; CCRIS tells you why.

Understanding Your CTOS Score

Your CTOS Score is more than a number — it’s a snapshot of your financial reliability. Your CTOS Report pulls together several layers of information:

- Banking payment history (CCRIS): Your credit accounts, outstanding balances and 12 months of repayment conduct, as reported by banks and financial institutions to Bank Negara’s Central Credit Reference Information System.

- Legal records: Any litigation, judgments or bankruptcy information sourced from public records.

- Directorships and business interests: Company directorships or business ownership tied to your name.

- Trade references: Payment behaviour reported by non-bank businesses you’ve transacted with.

How Is Your CTOS Score Calculated?

The CTOS Score runs from 300 to 850 and is built from five weighted factors. Knowing the weighting tells you where to focus your effort — payment history alone is nearly half the score:

| Factor | Weight | What it measures |

|---|---|---|

| Payment history | 45% | Whether you pay on time; how late you’ve been (30/60/90+ days); collections, defaults, legal action |

| Amounts owed | 20% | How much you owe and your credit utilisation (balances vs available limits) |

| Credit mix | 14% | The variety of credit you manage — cards, instalment loans, mortgage |

| New credit | 14% | How many new accounts/applications you’ve made recently |

| Length of credit history | 7% | How long you’ve used credit; age of your oldest and average accounts |

The single biggest lever is obvious: pay on time, every time. The second is keeping balances low relative to your limits.

What Is a Good CTOS Score?

CTOS groups scores into bands. A score of 697 and above is generally considered good, and many banks look for this range before approving unsecured credit. Here’s how the bands break down:

| CTOS Score | Rating | What it means for you |

|---|---|---|

| 744–850 | Excellent | Strong approval odds; best shot at the lowest rates |

| 718–743 | Very good | Seen as low-risk by most lenders |

| 697–717 | Good | Generally approvable for most products |

| 651–696 | Fair | May be approved, but with closer scrutiny |

| 529–650 | Low | Higher rejection risk; expect tougher terms |

| 300–528 | Poor | Approval is difficult; focus on rebuilding |

Important: there’s no universal cut-off. Each bank sets its own rules and also weighs your income, DSR (debt service ratio) and CCRIS conduct. A strong CTOS Score helps, but it’s not the only number lenders see. Before a major application like a home loan or car loan, it’s worth pulling your report a few months ahead so you have time to fix anything.

Improving Your CTOS Score

A stronger score opens doors to better rates and higher approval odds. Because payment history (45%) and amounts owed (20%) together make up two-thirds of the score, that’s where almost all your effort should go.

1. Pay Every Bill on Time

- Automate the minimum: Set up auto-debit for at least the minimum payment on every card and loan so a single missed due date never drags your score down.

- Use reminders for the rest: Calendar alerts a few days before each due date give you time to top up funds.

- Protect the essentials first: Loan instalments and card minimums are reported to CCRIS — prioritise these even in a tight month.

2. Manage Your Credit Utilisation

- Keep balances below 30% of your limit: High utilisation signals stress, even if you pay in full. Paying down before your statement date can help.

- Ask for a limit increase (carefully): A higher limit lowers your utilisation ratio if you don’t increase spending — but only request it if your repayment record is solid.

- Don’t max out cards: Running cards to the limit is one of the fastest ways to push the “amounts owed” component against you.

3. Be Strategic About New Applications

- Space out applications: New credit is 14% of the score. Several applications in a short window looks like cash-flow trouble. Avoid applying for multiple cards or loans at once.

- Keep older accounts open: Length of history counts (7%). Closing your oldest card can shorten your average account age — think twice before cancelling it.

- Keep a healthy mix: A blend of revolving (cards) and instalment (loans) credit, managed well, supports the 14% credit-mix component. Don’t open accounts just for variety, though.

4. Review and Dispute Errors

- Check regularly: Review your CTOS and CCRIS reports for inaccuracies — duplicate entries, settled accounts still showing as owing, or records that aren’t yours.

- File a dispute with evidence: You can raise a dispute through MyCTOS. Attach proof (receipts, settlement letters, bank statements). Under the Credit Reporting Agencies Act 2010, CTOS investigates and responds within 21 working days.

- Be patient with the source: Corrections happen at source — the bank, court or registry that supplied the data must update it. Because CCRIS refreshes monthly, even a confirmed fix can take a cycle to flow through to your score.

Read also: Best Personal Loans in Malaysia · Best Credit Cards in Malaysia

Overcoming Common CTOS Challenges

What to Do After a Loan Rejection

A rejection is frustrating, but it’s a chance to find and fix the weak spot:

- Ask why: Lenders won’t always volunteer it, but you can ask which factor weighed against you — score, DSR, or a CCRIS record.

- Pull your own reports: Check both CTOS and CCRIS for errors or a forgotten arrears entry that may have triggered the decline.

- Fix DSR, not just the score: Often the issue isn’t your score but your debt service ratio — too much existing debt relative to income. Paying down a balance or consolidating with a balance transfer can help.

- Rebuild, then reapply: Give it a few months of clean repayments before trying again, rather than applying repeatedly (which adds new-credit inquiries).

Recovering From a Default or AKPK Status

- Settle and get it documented: After clearing a default, obtain a letter confirming settlement and make sure it reflects in CCRIS/CTOS.

- Consider AKPK: The Credit Counselling and Debt Management Agency (AKPK), set up by Bank Negara, offers free debt-management help. Being under AKPK can affect new financing while active, but it’s a structured path back to stability.

- Stay consistent: Negative records age out over time; a steady run of on-time payments gradually outweighs old damage.

Frequently Asked Questions

Conclusion

Your CTOS Score shapes the financing you can access and the rates you’ll pay, but it isn’t a mystery and it isn’t fixed. Check it regularly — your CCRIS report is free from Bank Negara, and the full CTOS Score Report is a small fee well worth paying before any big application. Then focus where it counts: pay on time, keep balances low, space out new applications, and dispute genuine errors. Build those habits and your score will follow.

Disclaimer: This article is provided by KayaToday for general information only and is not financial advice. Credit-scoring criteria, report pricing and access methods change — always verify the latest details directly with CTOS and Bank Negara Malaysia before making decisions. Verified June 2026.