Calculate Your Loan Repayment Instantly

- Calculate Your Loan Repayment Instantly

- Fast Approval Personal Loans in Malaysia

- What “fast approval” actually means

- The big 2026 change: how interest is quoted

- Are there banks that offer fast loan approval?

- Banks and digital banks offering fast approval

- Non-bank and licensed moneylenders

- Top Fast Approval Personal Loans in Malaysia for 2026

- Quick answer: which fast loan is best for you?

- 1. GXBank FlexiCredit (digital bank — fastest end-to-end)

- 2. CIMB Cash Plus Personal Loan

- 3. Alliance Bank CashFirst Personal Loan

- 4. RHB Personal Financing

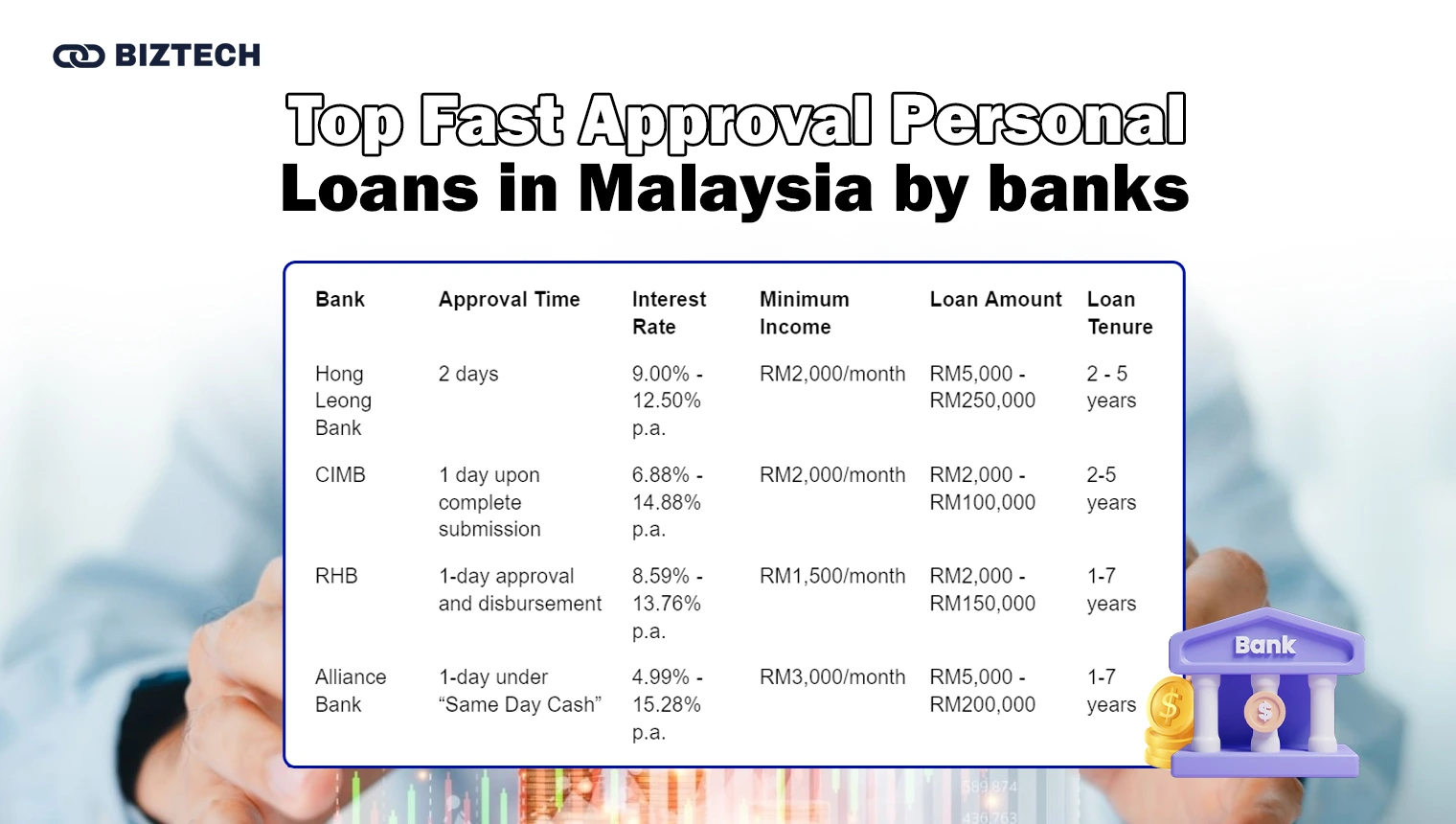

- 5. Hong Leong Personal Loan

- Top Fast Approval Personal Loans by non-banks

- 1. Icon Venture Capital

- 2. Emicro

- 3. Yayasan Ihsan Rakyat (civil servants)

- 4. JCL Credit Leasing

- 5. instaDuit

- Applying for a Fast Approval Personal Loan in Malaysia

- How to choose the right fast loan (5-step framework)

- Documents to prepare

- Step-by-step application

- Tips to improve your approval chances

- Common pitfalls to avoid

- Conclusion

- Frequently Asked Questions

Fast Approval Personal Loans in Malaysia

A fast approval personal loan is an unsecured loan where the application, credit assessment and disbursement are compressed into hours or a day or two, rather than the three-to-five working days a traditional personal loan can take. With digital banks and online lenders now competing aggressively, many Malaysians can get a decision in minutes and money in their account within one working day — provided their documents and credit record are in order.

One important reality check up front: “instant approval” almost always means an automated pre-approval or eligibility decision, not instant cash. Final approval still depends on document verification and a CCRIS/CTOS credit check, and the actual transfer can take a few hours to two working days. Treat the headline “approval in minutes” as the first step, not the finish line.

Figures below were verified in June 2026 against issuer pages and reputable comparison sites (RinggitPlus, iMoney). Rates, caps and promotions change often, so always confirm the final number with the lender before you sign.

What “fast approval” actually means

Speed comes from three things: a fully online application (no branch visit), automated income and credit verification, and instant disbursement into an account at the same bank. Once you submit, the lender assesses your credit history, income, employment type, existing commitments and debt service ratio (DSR) — the same criteria as any personal loan. Fast lenders simply automate these checks. The loan amount, rate and tenure you are offered still depend on your creditworthiness and ability to repay.

The big 2026 change: how interest is quoted

Bank Negara Malaysia (BNM) has overhauled how personal financing is priced. Under the revised Fair Treatment of Financial Consumers framework, the flat-rate method and the Rule of 78 are being phased out for new personal financing, and from 1 January 2027 all new personal loans must use the reducing-balance method — interest is charged only on what you still owe, not on the full original amount. Lenders must also disclose the Effective Interest Rate (EIR), the total repayment amount and the calculation method upfront, including in advertisements. Borrowing above RM100,000 will require a short financial-education module via the lender or AKPK.

Why this matters for fast loans: a “4.38% p.a.” flat rate is not the same as 4.38% on a normal mortgage-style loan. The true cost (EIR) is often roughly 1.8–2× the flat rate — CIMB Cash Plus, for example, advertises from 4.38% flat but an EIR of about 8.08%. Always compare loans on EIR, not the flat headline. The OPR sits at 2.75% (held at the May 2026 MPC), so funding costs — and therefore loan rates — have been broadly stable through 2026.

Are there banks that offer fast loan approval?

Yes — and the field has widened. Alongside the established banks (CIMB, Hong Leong, RHB, Alliance Bank, Maybank), digital banks such as GXBank and AEON Bank now offer end-to-end app-based applications with near-instant eligibility decisions. Most fast-approval personal loans no longer require a guarantor if you meet the income and credit-score thresholds.

Banks and digital banks offering fast approval

For salaried Malaysians with a clean credit record, the quickest routes are usually a loan from a bank where you already hold a payroll or savings account (because income can be verified instantly) or a digital bank that pulls your data electronically. CIMB, for instance, offers same-day approval to existing payroll/loan customers who apply via self-service, with disbursement within two working days.

Non-bank and licensed moneylenders

Beyond banks, licensed moneylenders and credit-leasing companies (regulated under the Moneylenders Act 1951 and licensed by KPKT) and digital lenders can approve in as little as a day. They are more flexible on credit history but charge materially more — the statutory ceiling for unsecured moneylender loans is 18% p.a. Always verify a non-bank’s licence on the KPKT register and the company on MyData SSM before applying, and never pay an “upfront processing fee” to release a loan — that is a hallmark of a loan scam.

Top Fast Approval Personal Loans in Malaysia for 2026

Here is an updated comparison of the fastest, most competitive personal loans in Malaysia for 2026. Rates shown are advertised flat rates unless noted; remember the EIR (true cost) is significantly higher.

| Lender | Approval / Disbursement | Rate (flat p.a.) | Indicative EIR | Min Income | Loan Amount | Tenure |

| GXBank FlexiCredit | Instant in-app eligibility; fast disbursement | from 3.78% | from ~6.45% | RM2,000/mo | up to RM150,000 | up to 5 yrs |

| CIMB Cash Plus | Same-day approval*; disburse ~2 working days | from 4.38% | 8.08% – 31.42% | RM2,000/mo | up to RM100,000 | up to 5 yrs |

| Alliance Bank CashFirst | Within 24 hrs (digital / TNG GoFinance) | 4.99% – 16.68% | from ~7.40% | RM3,000/mo | up to RM200,000 | up to 7 yrs |

| RHB Personal Financing | Instant approval; quick disbursement | from ~7.62% | verify with RHB | RM1,500–2,000/mo | up to RM150,000 | up to 7 yrs |

| Hong Leong Personal Loan | ~2 working days | from ~9.00% | verify with HLB | RM2,000/mo | up to RM250,000 | up to 5 yrs |

*CIMB same-day approval is limited to customers holding a CIMB payroll or loan account who apply via self-service submission; the 4.38% flat rate applies to CIMB Preferred customers and is subject to approval.

Quick answer: which fast loan is best for you?

| If you want… | Best fast option | Why |

| A fully app-based, paperless loan | GXBank FlexiCredit | Digital-bank onboarding, instant eligibility, low headline rate |

| Lowest advertised rate (existing CIMB customer) | CIMB Cash Plus | From 4.38% flat, same-day approval for payroll customers |

| A larger amount and longer tenure | Alliance CashFirst / Hong Leong | Up to RM200k–RM250k, tenure up to 7 years |

| Lower income threshold | RHB Personal Financing | Accepts income from around RM1,500–2,000/month |

| Shariah-compliant fast financing | Alliance CashVantage-i / Bank Islam-i | Profit-rate based, no conventional interest |

1. GXBank FlexiCredit (digital bank — fastest end-to-end)

GXBank, Malaysia’s first licensed digital bank, offers FlexiCredit entirely through its app. Eligibility is assessed instantly and approved applicants can draw down quickly, making it one of the fastest genuinely paperless options in 2026.

- Rate: from 3.78% p.a. flat (EIR from ~6.45%), depending on profile and tenure

- Loan amount: up to RM150,000

- Tenure: up to 5 years

- Min income: around RM2,000/month

- Best for: borrowers comfortable with an app-only process who want speed and a low headline rate

Confirm the exact rate offered to you in-app — digital-bank pricing is personalised and changes frequently.

2. CIMB Cash Plus Personal Loan

CIMB Cash Plus is one of the most popular fast loans because the online form takes about 10 minutes and existing CIMB payroll/loan customers can receive same-day approval, with funds disbursed within two working days.

Worked example (flat-rate basis): Borrow RM10,000 over 2 years at 4.38% p.a. flat → interest RM876 total → monthly repayment roughly RM453. On an EIR basis (~8.08%) the true cost is higher — always check the EIR figure CIMB discloses.

- Rate: from 4.38% p.a. flat (EIR 8.08%–31.42% depending on profile); 4.38% applies to CIMB Preferred customers

- Loan amount: up to RM100,000

- Tenure: up to 5 years

- Min income: RM2,000/month; age 21–58

- Fees: no processing fee; no stamp duty on the loan; late penalty 1% p.a. of the outstanding amount

- Documents: IC, latest 1–3 months’ payslips, EPF statement (min 6 months); self-employed add business registration and 6-month bank statements

3. Alliance Bank CashFirst Personal Loan

Alliance Bank’s CashFirst is built for speed: applications via the bank’s website or the Touch ‘n Go eWallet GoFinance channel can be approved and disbursed within 24 hours. A Shariah-compliant version, CashVantage Personal Financing-i, offers the same profit-rate range.

- Rate: 4.99% – 16.68% p.a. flat (EIR from ~7.40%)

- Loan amount: up to RM200,000

- Tenure: up to 7 years

- Min income: from RM3,000/month; age 21–60

- Fees: no processing fee, no early-settlement fee; only stamp duty of 0.5% (deducted from the disbursed amount)

- Documents: IC, latest 3 months’ payslips or bank statements; self-employed add SSM registration and income-tax documents

4. RHB Personal Financing

RHB offers instant approval and quick disbursement of up to RM150,000 through RHB Personal Financing, with one of the lower income thresholds among the banks — helpful if you earn closer to RM1,500–2,000 a month.

- Rate: from ~7.62% p.a. (confirm flat vs EIR with RHB)

- Loan amount: up to RM150,000

- Tenure: up to 7 years

- Min income: from around RM1,500–2,000/month; age 21–60

- Fees: stamp duty 0.5%; late penalty 1% of outstanding; early-settlement terms apply (confirm any lock-in)

- Documents: IC, latest 3 months’ payslips or EPF/bank statements; self-employed add business registration and tax receipts

5. Hong Leong Personal Loan

Hong Leong Bank offers fast approval (typically around two working days) with the largest headline ceiling on this list — up to RM250,000 — suited to bigger financing needs where a day or two extra is acceptable.

- Rate: from ~9.00% p.a. (confirm flat vs EIR with HLB)

- Loan amount: up to RM250,000

- Tenure: up to 5 years

- Min income: RM2,000/month; age 21–60

- Fees: no processing fee; stamp duty 0.5%; no early-termination charge with 3 months’ written notice; late penalty 1% of outstanding

- Documents: IC (front and back), latest 3 months’ payslips or 6-month bank statements; EPF/tax documents for self-employed

Top Fast Approval Personal Loans by non-banks

If a bank declines you or you need money in a single day, licensed moneylenders and credit-leasing companies are an alternative — but they cost more, so treat them as a last resort and read the contract carefully. The figures below are indicative; verify each lender’s KPKT licence and current terms before applying.

| Lender | Approval Time | Rate | Min Income | Regulator |

| Icon Venture Capital | 1 day | 18% p.a. | RM3,000/mo | Moneylenders Act 1951 |

| Emicro | 1 day (as fast as 6 hours) | 18% p.a. | RM1,500/mo | KPKT |

| Yayasan Ihsan Rakyat | 1 day | 5.99% – 9.99% p.a. | RM1,500/mo | Civil servants only |

| JCL Credit Leasing | ~3 days | 18% – 20% p.a. | RM1,000/mo | Credit-leasing licensee |

| instaDuit (BB Capital) | 1 day | 18% p.a. | RM1,500/mo | KPKT (WL6540) |

Important: a legitimate licensed moneylender will never ask you to pay a fee before releasing your loan, will issue a proper agreement (Schedule J / borrower’s copy), and will be searchable on the KPKT moneylender register. If any “lender” demands an upfront deposit, processing fee or “GST clearance” payment via e-wallet before disbursing, it is a scam — stop and report it.

1. Icon Venture Capital

A high-margin personal loan from Icon Venture Capital Sdn Bhd (Company No. 1246743-K), licensed under the Moneylenders Act 1951.

| Amount | Loan period | Min income | Rate |

| RM5,000 – RM100,000 | 12 to 60 months | Min. RM36,000/yr | 18% p.a. |

Fees & charges: rate from 18% p.a.; no processing fee; no stamp duty; early-termination charges 6 months’ interest; late penalty 8% of outstanding. Eligibility: min annual income RM36,000; age 18–60; Malaysians residing in Klang Valley only (salaried or self-employed). Documents: application form, IC (both sides), latest 3 months’ payslips and bank statements, latest EPF/BE form, utility bill and proof of address.

2. Emicro

Emicro Services Sdn Bhd is a KPKT-licensed micro-financier offering small, fast loans to Malaysians, with disbursement in as little as 6 hours (next working day if applied outside working hours). A CIMB account is recommended for fastest deposit.

| Amount | Loan period | Min income | Rate |

| RM500 – RM1,000 | 1 to 3 months | Min. RM18,000/yr | 18% p.a. |

| RM1,001 – RM3,000 | 1 to 6 months | Min. RM24,000/yr | 18% p.a. |

| RM3,001 – RM5,000 | 1 to 12 months | Min. RM36,000/yr | 18% p.a. |

| RM5,001 – RM10,000 | 1 to 24 months | Min. RM48,000/yr | 18% p.a. |

Fees & charges: rate from 18% p.a.; processing fee RM60 up to a max of RM400; stamp duty included in processing fee; no early-termination fee; late penalty RM25 or 8% of outstanding. Eligibility: min annual income RM18,000; age 18–50; Malaysians (salaried or self-employed). Emicro does not approve applications from certain government/uniformed roles, factory operators, sales promoters, drivers and commission-only earners. Documents: IC (both sides), selfie holding MyKad, latest payslip or EPF statement, utility bill.

3. Yayasan Ihsan Rakyat (civil servants)

YIR (incorporated 2012, registration 1003231-A) offers fixed-rate Islamic personal financing to Malaysian civil servants of selected employers only (Accountant General, PDRM, UPM, UiTM).

| Amount | Loan period | Min income | Rate |

| RM2,500 – RM250,000 | 12 to 120 months | Min. RM18,000/yr | 5.99% – 9.99% p.a. |

Fees & charges: rate from 5.99% p.a.; no processing fee; stamp duty 0.5%; early-termination fee RM100; late penalty 1% of outstanding. Eligibility: Malaysian civil servant of an eligible employer, age 20–50 (PDRM up to 55), gross income from RM1,500/month, permanent job with 6+ months’ service, not bankrupt, pass YIR credit assessment. Documents: MyKad/PDRM ID, recent 3 months’ payslips, latest bank statement, employment verification letter (and option/transfer/settlement letters if applicable).

4. JCL Credit Leasing

JCL i-Fund is an unsecured Islamic personal loan from a licensed credit-leasing company, with approval in as fast as three working days.

| Amount | Loan period | Min income | Rate |

| RM1,000 – RM50,000 | 6 to 60 months | Min. RM12,000/yr | 18% – 20% p.a. |

Fees & charges: rate from 18% p.a.; processing fee RM50; no stamp duty; no early-termination fee; late charge 1% Ta’widh + 7% Gharamah per annum on the amount due. Eligibility: min annual income RM12,000; age 18–60; Malaysians in Klang Valley, Penang, Johor, Ipoh, Kedah and Kelantan (salaried, self-employed or commission). Documents (salaried): IC (both sides), latest 3 months’ payslips and bank statement, latest utility bill. Self-employed: IC, latest SSM, 6-month company and 3-month personal bank statements, utility bill.

5. instaDuit

Offered by BB Capital Sdn Bhd, instaDuit is a KPKT-licensed online lender (registration WL6540/10/01-4/151122) promising approval within 24 hours.

| Amount | Loan period | Min income | Rate |

| RM1,000 – RM10,000 | 12 to 48 months | Min. RM18,000/yr | 18% p.a. |

Fees & charges: rate from 18% p.a.; processing fee per loan agreement; stamp duty 0.5%; early-termination fee per agreement; late penalty 8% of outstanding. Eligibility: min annual income RM18,000 (min salary RM1,500/month); age 21–55; Malaysian salaried employees working in KL, Selangor or Putrajaya; not bankrupt; not under AKPK’s debt-management programme. Documents: selfie, IC (front and back), latest 3 months’ payslips and salary-account bank statements, latest EPF statement, utility bill.

Applying for a Fast Approval Personal Loan in Malaysia

Speed is mostly within your control. The biggest delays in “fast” loans come from missing documents, an income that can’t be verified instantly, or a borderline DSR. Prepare properly and the automated systems can do the rest.

How to choose the right fast loan (5-step framework)

- Compare on EIR, not flat rate. A 4.38% flat loan can cost ~8% EIR. Use the disclosed EIR (now mandatory) to compare like-for-like.

- Borrow only what you need. A smaller loan over a shorter tenure costs far less in total interest, even at the same rate.

- Check your DSR before applying. Most banks want your total commitments (including the new loan) below roughly 60–70% of net income. A high DSR is the most common reason a “fast” approval stalls.

- Apply where your money already is. A loan from your payroll/salary-crediting bank verifies income instantly — often the genuine same-day route.

- Read the fees, not just the rate. Stamp duty (0.5%), early-settlement terms and late penalties affect the real cost. No-processing-fee + no-early-exit-fee loans (e.g. Alliance CashFirst) are friendlier if you may repay early.

Documents to prepare

| Salaried Employee | Self-Employed |

| IC (front and back); latest 3–6 months’ payslips; latest 3–6 months’ EPF statement; latest BE/e-BE form with tax receipt; latest EA form | IC (front and back); SSM business registration; latest 3–6 months’ bank statements; latest BE/e-BE form with tax receipt; 6-month commission statements (commission earners) |

Step-by-step application

- Compare: use comparison sites such as RinggitPlus and CompareHero, or our own best personal loans guide and personal loan calculator.

- Apply online: complete the lender’s digital form (10–15 minutes for most banks).

- Submit documents: upload exactly what’s requested — incomplete files are the #1 cause of delay.

- Approval & disbursement: automated pre-approval can be minutes; final disbursement ranges from a few hours to two working days.

Tips to improve your approval chances

1. Keep your DSR healthy. DSR = (total monthly commitments ÷ net income) × 100. Example: net income RM7,000, existing commitments RM1,500, new loan repayment RM1,000 → DSR = (RM2,500 ÷ RM7,000) × 100 = 35.7%. Staying in a comfortable band well below the bank’s ceiling makes a fast “yes” far more likely.

2. Pay on time, in full. A clean repayment record in your CCRIS report is the single biggest lever on approval speed. Check it before you apply — see our guide on how to check your CTOS/CCRIS score.

3. Fix a weak credit score first. Clear any past-due amounts and let a few months of clean payments register before applying.

4. Reduce or consolidate existing debt. Lower commitments improve your DSR. A balance transfer can also cut what you pay on existing card debt.

5. Build a credit history (beginners). If you have no track record, a small credit card or loan, repaid on time, creates the history lenders look for.

Common pitfalls to avoid

- Confusing flat rate with EIR. The advertised flat rate understates the true cost by roughly 1.8–2×.

- Assuming “instant approval” = instant cash. Verification and disbursement still take time.

- Stretching the tenure to lower the monthly payment. A longer tenure means much more total interest.

- Upfront-fee scams. No legitimate lender requires payment before releasing your loan.

- Borrowing from unlicensed “Ah Long” operators. Always confirm the KPKT licence and the company on SSM.

Conclusion

Fast approval personal loans are a genuine lifeline in an emergency, and 2026 has made them faster and more transparent — digital banks compress the process to minutes, and BNM’s move to reducing-balance pricing and mandatory EIR disclosure (fully from January 2027) makes the true cost easier to see. The smart approach is the same as for any borrowing: take only what you need, compare on EIR, keep your DSR in check, and read the fees before you sign. Used responsibly, a fast loan solves a short-term problem without creating a long-term one.

Disclaimer: This guide is provided by KayaToday for general information only and is not financial advice. Rates, fees and eligibility were verified in June 2026 but change frequently — always confirm the latest terms directly with the lender before applying.

Frequently Asked Questions

![Malaysia Best Fixed Deposit Rates [July 2026]](https://kayatoday.com/wp-content/uploads/2025/07/Best-Fixed-Deposit-Rate-Malaysia-300x170.jpg)