Calculate Your Loan Repayment Instantly

- Calculate Your Loan Repayment Instantly

- Quick Answer: Best Housing Loan in Malaysia (2026)

- Understanding Housing Loans in Malaysia

- How Malaysian Home Loan Rates Actually Work (SBR + Spread)

- OPR in 2026: Where Rates Stand

- 2026 Home Loan Rate Comparison: Malaysia’s Major Banks

- Fixed vs Floating: Which Should You Choose?

- Types of Housing Loan in Malaysia

- How to Choose the Right Housing Loan: A 5-Step Framework

- Worked Example: RM450,000 Loan Over 30 Years

- First-Time Buyer Schemes & 2026 Incentives

- Best Housing Loans for Refinancing

- Best Islamic Housing Loans

- How to Improve Your Chances of Loan Approval

- 1. Check and clean up your credit

- 2. Manage your Debt Service Ratio (DSR)

- 3. Show stable income and savings

- Common Pitfalls to Avoid

- What Documents Do I Need to Apply?

- Summary

- Frequently Asked Questions (FAQs)

Choosing the best housing loan in Malaysia in 2026 comes down to one number that every bank now shares – the Standardised Base Rate (SBR) – plus the spread each lender adds on top. With Bank Negara Malaysia (BNM) holding the Overnight Policy Rate (OPR) at 2.75% since the July 2025 cut, effective home loan rates for well-qualified borrowers currently sit between roughly 4.22% and 4.35% p.a. This guide explains exactly how the rate is built, compares the major banks, walks through a real repayment example, and shows you how to qualify for the lowest spread. Figures verified June 2026 – always confirm the live rate with the bank, as your offered spread depends on your credit profile.

Quick Answer: Best Housing Loan in Malaysia (2026)

| You want… | Best pick (2026) | Why |

|---|---|---|

| Lowest effective rate | Public Bank | Consistently the lowest spread (~SBR + 1.47% ≈ 4.22%) |

| Zero / low down payment | Skim Rumah Pertamaku (SRP) | Up to 110% financing for first-timers earning ≤RM5,000/mo |

| Rent-to-own flexibility | Maybank HouzKEY | No upfront down payment; step-up instalments from ~2.88% |

| Flexi loan / park savings | Hong Leong, Maybank, Public Bank Flexi | Offset extra cash against principal, withdraw anytime |

| Islamic financing | Bank Islam, Maybank Islamic | Musharakah Mutanaqisah / Tawarruq, profit rate ≈ 4.30% |

| Refinancing | Public Bank, Hong Leong | Competitive spreads + low/zero legal fees on selected packages |

Rates are indicative best-available rates for borrowers with a clean CCRIS record and DSR under 60%. Your actual offer may be higher.

Understanding Housing Loans in Malaysia

A housing loan (home loan or mortgage) is financing that a bank provides so you can buy a property, repaid over a long tenure – commonly up to 35 years or until age 70, whichever comes first. In Malaysia, almost every home loan is a floating-rate loan: your interest rate moves up or down whenever BNM changes the OPR. There is no US-style 30-year fixed mortgage here. Understanding that single fact – that your repayment can change – is the foundation of borrowing responsibly.

How much you can borrow depends on your income, your existing debts (measured by your Debt Service Ratio), your credit standing in CCRIS and CTOS, and the bank’s valuation of the property. Most banks finance up to 90% of the property price for your first two homes (the margin of finance), with the remaining 10% plus legal and stamp duty costs paid upfront.

How Malaysian Home Loan Rates Actually Work (SBR + Spread)

Since 1 August 2022, BNM replaced the old Base Rate (BR) system with the Standardised Base Rate (SBR) for all new retail floating-rate loans. The key point: every bank shares the same SBR, because it is pegged 1:1 to the OPR. Your effective rate is built like this:

Effective Rate = SBR (2.75%) + the bank’s Spread

The spread is the only part banks compete on. It reflects your credit risk, the loan-to-value ratio and the bank’s strategy. A package advertised as “SBR + 1.50%” works out to 4.25% p.a. today. If BNM cuts the OPR, your SBR – and your monthly instalment – falls automatically; if it hikes, your payment rises. If anyone still quotes you a “BLR” or “BR” figure, they are describing a legacy pre-2022 loan.

OPR in 2026: Where Rates Stand

BNM cut the OPR from 3.00% to 2.75% in July 2025 – its first reduction since the 2020 pandemic cuts – describing it as a pre-emptive buffer against global trade uncertainty rather than the start of an easing cycle. The Monetary Policy Committee meets six times a year and has held at 2.75% at every meeting since, including through the first half of 2026. With headline inflation running around 1.4–1.7%, most economists expect the OPR to stay at 2.75% through 2026, with only a small chance of a further 0.25% cut. No analyst is currently forecasting a hike – a relatively favourable window for new borrowers.

2026 Home Loan Rate Comparison: Malaysia’s Major Banks

All six of the largest mortgage lenders share the same 2.75% SBR – the differences below come entirely from each bank’s spread. The monthly instalment is calculated on a RM500,000 loan over a 30-year tenure.

| Bank | SBR | Typical spread | Effective rate | Est. instalment (RM500k/30yr) | Notes |

|---|---|---|---|---|---|

| Public Bank | 2.75% | +1.47% | ~4.22% | ~RM2,451 | Consistently the lowest spread |

| Hong Leong Bank | 2.75% | +1.53% | ~4.28% | ~RM2,468 | Competitive above RM500k; strong Flexi |

| Maybank | 2.75% | +1.55% | ~4.30% | ~RM2,474 | Largest mortgage book; HouzKEY rent-to-own |

| Bank Islam | 2.75%* | +1.55% | ~4.30% | ~RM2,474 | Islamic base financing rate (SBR-equivalent) |

| RHB Bank | 2.75% | +1.57% | ~4.32% | ~RM2,480 | Aggressive on refinancing packages |

| CIMB Bank | 2.75% | +1.60% | ~4.35% | ~RM2,489 | Highest spread among the Big 6 |

*Bank Islam uses an Islamic Base Financing Rate that functions like the SBR for comparison. Spreads shown are typical for a first property and good credit; confirm your offer with the issuer. Source: bank published rates and BNM, June 2026.

The gap looks small – just 0.13% between Public Bank and CIMB – but over 30 years on a RM500,000 loan that difference adds up to roughly RM13,700 in extra interest. Spending 30 minutes comparing spreads is one of the highest-value hours in the entire home-buying process.

Fixed vs Floating: Which Should You Choose?

Nearly all Malaysian home loans float with the SBR. A handful of banks offer “fixed-rate” packages, but they are only fixed for a promotional 3–5 years before reverting to floating, and they carry a premium of roughly 0.50%–1.00% – typically 4.75%–5.25% today.

| Feature | Floating rate | Fixed rate (promo) |

|---|---|---|

| Rate basis | SBR + spread (moves with OPR) | Fixed 3–5 yrs, then reverts to floating |

| Typical rate (2026) | 4.22%–4.35% | 4.75%–5.25% |

| Best for | Most buyers; benefit if OPR falls | Those who need short-term payment certainty |

| Availability | All banks | Limited, often promotional |

With the OPR expected to hold or possibly fall in 2026, paying a premium for temporary certainty rarely makes mathematical sense for most borrowers. A semi-flexi or flexi floating loan is the default choice for the vast majority.

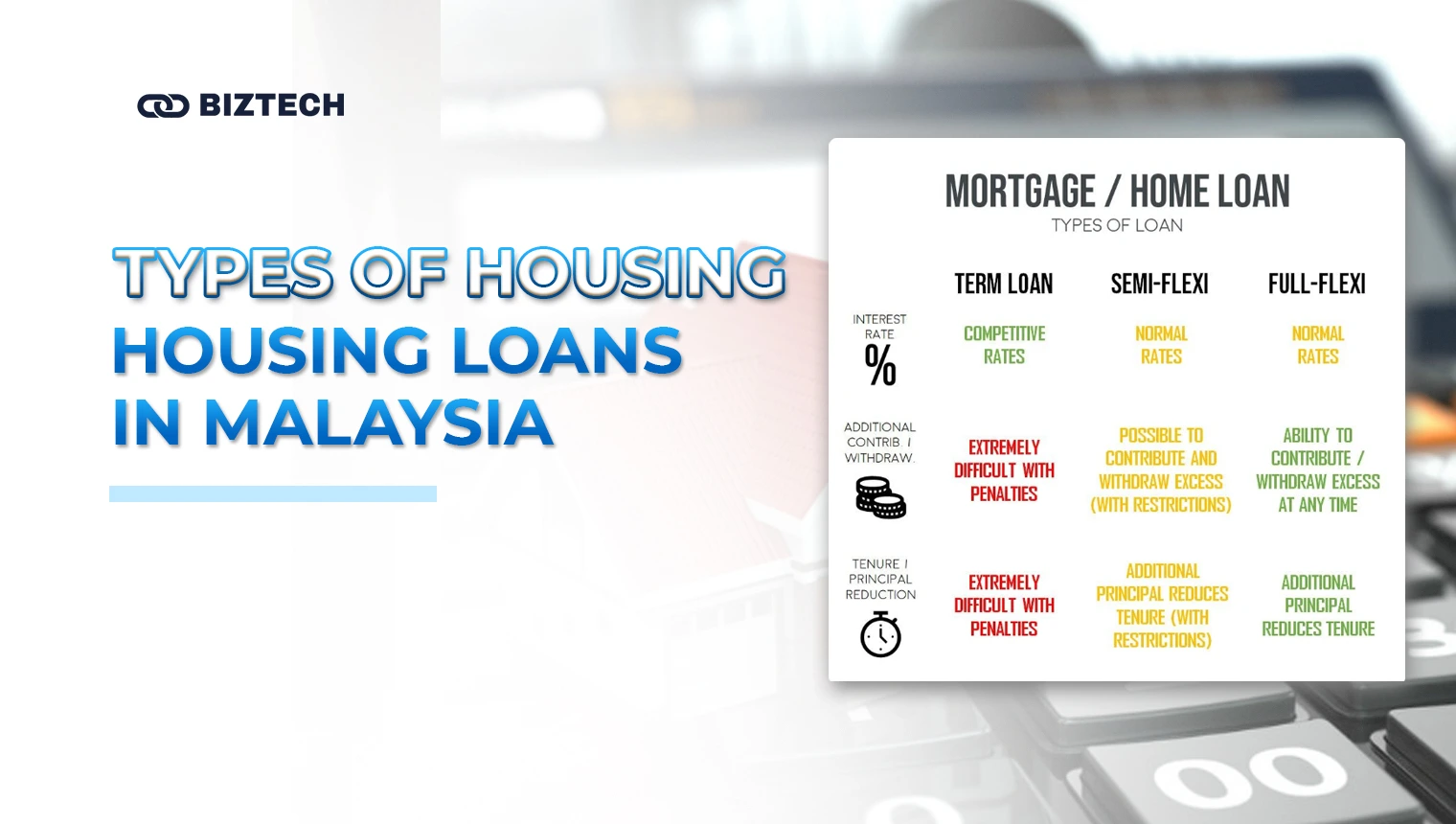

Types of Housing Loan in Malaysia

Beyond the rate, the loan structure decides how much flexibility you have to save on interest:

- Term Loan: The simplest structure – a fixed repayment schedule with the same instalment each month. Best for borrowers who want predictability and won’t make extra payments.

- Semi-Flexi Loan: Lets you make extra payments to reduce principal and interest, but withdrawing that money back requires a request and sometimes a fee. The most popular balance of flexibility and low cost.

- Flexi Loan: Linked to a current account – any cash you park reduces the interest charged daily, and you can withdraw it instantly. Ideal if you keep a cash buffer or have variable income, though it may carry a small monthly maintenance fee.

A worked example: parking RM50,000 in a flexi account against a RM500,000 loan at 4.30% saves you roughly RM2,150 in interest in the first year alone – while keeping that cash fully accessible.

How to Choose the Right Housing Loan: A 5-Step Framework

Rate is only one variable. Use this order of priorities when comparing offers:

- Compare the spread, not the SBR. Every bank has the same 2.75% SBR – ask each banker for their lowest spread for your profile and get it in writing.

- Match the loan type to your habits. If you’ll keep spare cash, a flexi/semi-flexi loan beats a slightly cheaper term loan. If you want set-and-forget, a term loan is fine.

- Add up the real cost. Factor in legal fees, valuation, MRTA/MLTA insurance and any lock-in penalty – some banks waive legal fees, which can outweigh a 0.05% rate difference.

- Stress-test at +0.50%. Can you still afford the instalment if the OPR rises 0.50%? On a RM500k loan that is about RM140/month more. If not, borrow less.

- Check the lock-in period. Most packages lock you in for 3–5 years; selling or refinancing early triggers a penalty (often 2–3% of the loan).

Worked Example: RM450,000 Loan Over 30 Years

Say you buy a RM500,000 home, put down 10% (RM50,000) and borrow RM450,000 over 30 years at an effective 4.30% p.a.:

| Item | Amount |

|---|---|

| Loan amount | RM450,000 |

| Effective rate | 4.30% p.a. (SBR 2.75% + 1.55%) |

| Tenure | 30 years (360 months) |

| Monthly instalment | ~RM2,227 |

| Total interest over 30 yrs | ~RM351,700 |

| If rate rises to 4.80% | ~RM2,361/mo (+RM134/mo) |

The lesson: every 0.25% movement in the OPR shifts your payment by roughly RM65–RM70 per RM500,000 borrowed. Build that buffer into your budget before you commit. You can model your own numbers with our loan calculator guide.

First-Time Buyer Schemes & 2026 Incentives

If you have never owned a home, several government measures can dramatically cut your upfront cost in 2026:

- Skim Rumah Pertamaku (SRP / My First Home Scheme): Administered by Cagamas, it offers up to 110% financing – no down payment, with the extra 10% covering legal and moving costs. Eligibility: Malaysian, first property, aged 21–40, monthly income ≤RM5,000 (single) or ≤RM10,000 (joint), property priced ≤RM500,000.

- Stamp duty exemption (extended to 31 December 2027): First-time Malaysian buyers pay no stamp duty on both the property transfer (MOT) and the loan agreement for homes priced up to RM500,000 – a saving of around RM11,000 on a RM500,000 home. Homes above RM500,000 do not qualify.

- Skim Jaminan Kredit Perumahan (SJKP): Strengthened in Budget 2026 with RM20 billion in guarantees, now extended to applicants without fixed income such as gig workers, freelancers and the self-employed.

- Maybank HouzKEY: A rent-to-own option requiring no upfront down payment, with step-up instalments – useful if you have steady income but limited savings.

Building or repairing your credit first makes all of these easier to secure – start by learning how to check and improve your CTOS score.

Best Housing Loans for Refinancing

If you took your loan during the 2022–2023 rate-hike cycle and your lock-in has expired, refinancing could lower your spread. Public Bank and Hong Leong are frequently the most competitive, while RHB is aggressive on refinancing packages. Before switching, weigh the legal fees, valuation and any remaining lock-in penalty against the interest saved – refinancing only makes sense if your current effective rate is meaningfully above ~4.35% and you plan to keep the property for several more years.

Best Islamic Housing Loans

Shariah-compliant home financing in Malaysia delivers a similar monthly payment to conventional loans but rests on a different legal contract – there is no “interest”, only profit sharing or deferred-sale arrangements:

- Bank Islam Home Financing-i: Based on Tawarruq / Murabahah, with a base financing rate equivalent to the SBR (~4.30% effective) and flexible tenures.

- Maybank Islamic Home Financing-i: Uses Musharakah Mutanaqisah (diminishing partnership), competitive profit rates and flexi options.

- RHB Islamic Home Financing-i: Shariah-compliant financing with competitive profit rates and online application.

How to Improve Your Chances of Loan Approval

1. Check and clean up your credit

Your CCRIS (BNM) and CTOS records are the first thing a bank pulls. Pay every bill and existing loan on time, keep credit-card utilisation below 30%, settle or reduce outstanding debts, and avoid applying for multiple new loans in the months before your mortgage application. A clean record earns you a lower spread, not just approval. See our guide on checking and improving your credit score.

2. Manage your Debt Service Ratio (DSR)

Your DSR is the share of net monthly income committed to debt repayments, including the new mortgage. Calculate it as (total monthly debt ÷ net monthly income) × 100. Most banks want a DSR below 60–70%. Clearing a car loan or consolidating personal debt before you apply can lift the loan amount you qualify for. Compare ongoing commitments such as your car loan against your housing budget.

3. Show stable income and savings

Lenders favour applicants with at least two years in the same employment, or two to three years of consistent records if self-employed. Keep your payslips, EPF statements, bank statements and tax returns ready, and supporting assets such as fixed deposits or ASB certificates can strengthen your case – consider parking your deposit in a high-rate fixed deposit while you shop for a home.

Common Pitfalls to Avoid

- Comparing SBR instead of spread. The SBR is identical at every bank – the spread is what differs. Always ask for the effective rate.

- Ignoring the lock-in period. Selling or refinancing within the first 3–5 years usually triggers a 2–3% penalty.

- Maxing out your DSR. Borrowing the absolute maximum leaves no room for a rate rise – stress-test at +0.50%.

- Forgetting upfront costs. Legal fees, valuation, MRTA/MLTA and the 10% down payment can add up to 12–15% of the price on a non-exempt purchase.

- Overlooking flexi savings. If you keep idle cash, a flexi loan can save thousands in interest that a cheaper term loan cannot.

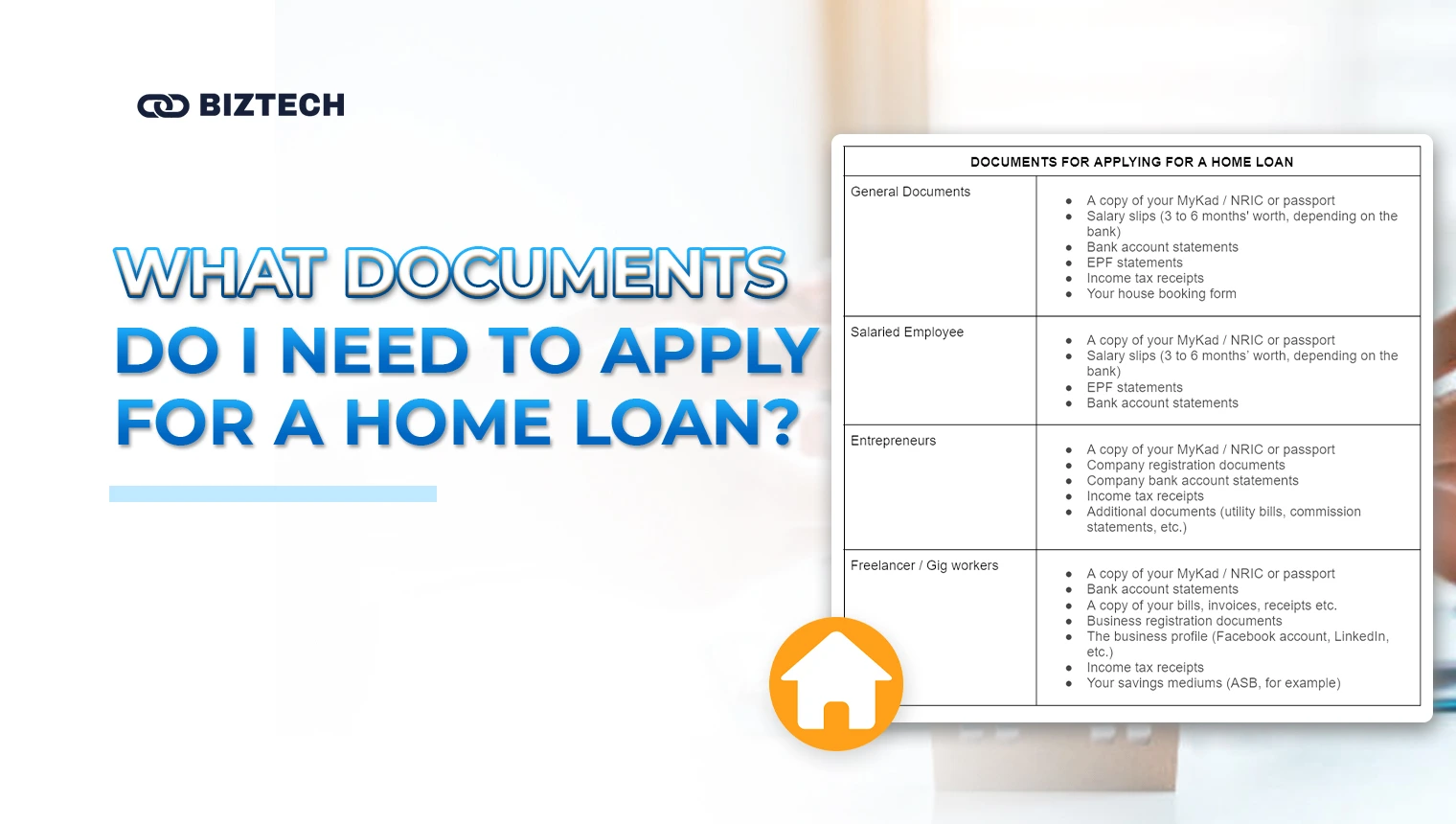

What Documents Do I Need to Apply?

Have these ready to speed up approval. You can also include fixed deposit certificates, ASB or Tabung Haji statements and bonds, which can improve your chances.

| Applicant type | Documents required |

|---|---|

| General (all applicants) | MyKad/NRIC or passport copy; 3–6 months’ salary slips; bank statements; EPF statement; income tax receipts (BE/B form); property booking form / SPA |

| Salaried employee | MyKad copy; 3–6 months’ salary slips; latest EPF statement; 3–6 months’ bank statements |

| Self-employed / Entrepreneur | MyKad copy; SSM company registration; company bank statements; income tax receipts; utility bills / commission statements |

| Freelancer / Gig worker | MyKad copy; 6–12 months’ bank statements; invoices/receipts; business registration; income tax receipts; savings proof (e.g. ASB) |

Summary

In 2026, the best housing loan in Malaysia is the one with the lowest spread for your credit profile and the right structure for your cash habits. Every bank shares the same 2.75% SBR, so effective rates cluster between 4.22% (Public Bank) and 4.35% (CIMB) for strong applicants. First-time buyers should layer on the SRP 110% financing, the stamp duty exemption (to end-2027) and SJKP guarantees to slash upfront costs. Compare spreads in writing, choose a flexi or semi-flexi loan if you keep spare cash, stress-test at +0.50%, and clean up your credit before applying. Always confirm the live rate and terms directly with the bank.

For authoritative reference, see Bank Negara Malaysia’s base rates page and its OPR decisions.

Read more: Best Fast Approval Personal Loans in Malaysia

Frequently Asked Questions (FAQs)

Disclaimer: This article is provided by KayaToday for general information only and is not financial advice. Interest/profit rates, spreads, eligibility and government schemes were verified in June 2026 but can change at any time – always confirm the latest terms directly with the bank or issuer before applying.

![Malaysia Best Fixed Deposit Rates [July 2026]](https://kayatoday.com/wp-content/uploads/2025/07/Best-Fixed-Deposit-Rate-Malaysia-300x170.jpg)