Calculate Your Loan Repayment Instantly

- Calculate Your Loan Repayment Instantly

- AEON iCASH Personal Financing: Loan up to RM100,000, Repay Over 7 Years

- Quick Answer: Is AEON iCASH Right for You?

- Table of Profit Rates (RM1,000 – RM100,000)

- Big 2026 Change: Flat Rate & Rule of 78 Are Being Phased Out

- Benefits & Features

- Eligibility

- Documents Required

- Fees and Charges

- Worked Example: What RM10,000 Over 5 Years Really Costs

- How to Decide If AEON iCASH Is Your Best Option

- Common Pitfalls to Avoid

- Alternative: AEON Bank Personal Financing-i (Fully Digital)

- Frequently Asked Questions

AEON iCASH Personal Financing: Loan up to RM100,000, Repay Over 7 Years

AEON Credit Service (M) Berhad offers several aeon credit personal loans, from insurance and takaful to financing. The one we cover here is the AEON iCASH Personal Financing-i — a Shariah-compliant (Tawarruq) personal financing facility you can use for bills, emergencies, debt consolidation, or any lawful purpose. You can borrow from RM1,000 up to RM100,000 and repay this aeon loan at your own pace over 6 to 84 months (up to 7 years), with no guarantor, no collateral, and no security deposit.

Figures below verified June 2026 against AEON Credit’s published rates and product disclosure sheet. Profit rates, fees, and eligibility can change — always confirm with AEON Credit before applying.

Quick Answer: Is AEON iCASH Right for You?

| If you… | AEON iCASH verdict |

|---|---|

| Earn from RM1,500/month and a bank rejected you | Strong fit — lower income bar than most banks |

| Need cash within days, even on a weekend | Strong fit — fast approval, 7-day-a-week disbursement |

| Qualify for a bank personal loan at 4–8% flat | Compare first — bank rates are usually cheaper |

| Want the lowest 0.66%/month rate | Depends — best rate is for strong profiles only |

| Prefer a fully app-based digital application | Consider AEON Bank Personal Financing-i instead (see below) |

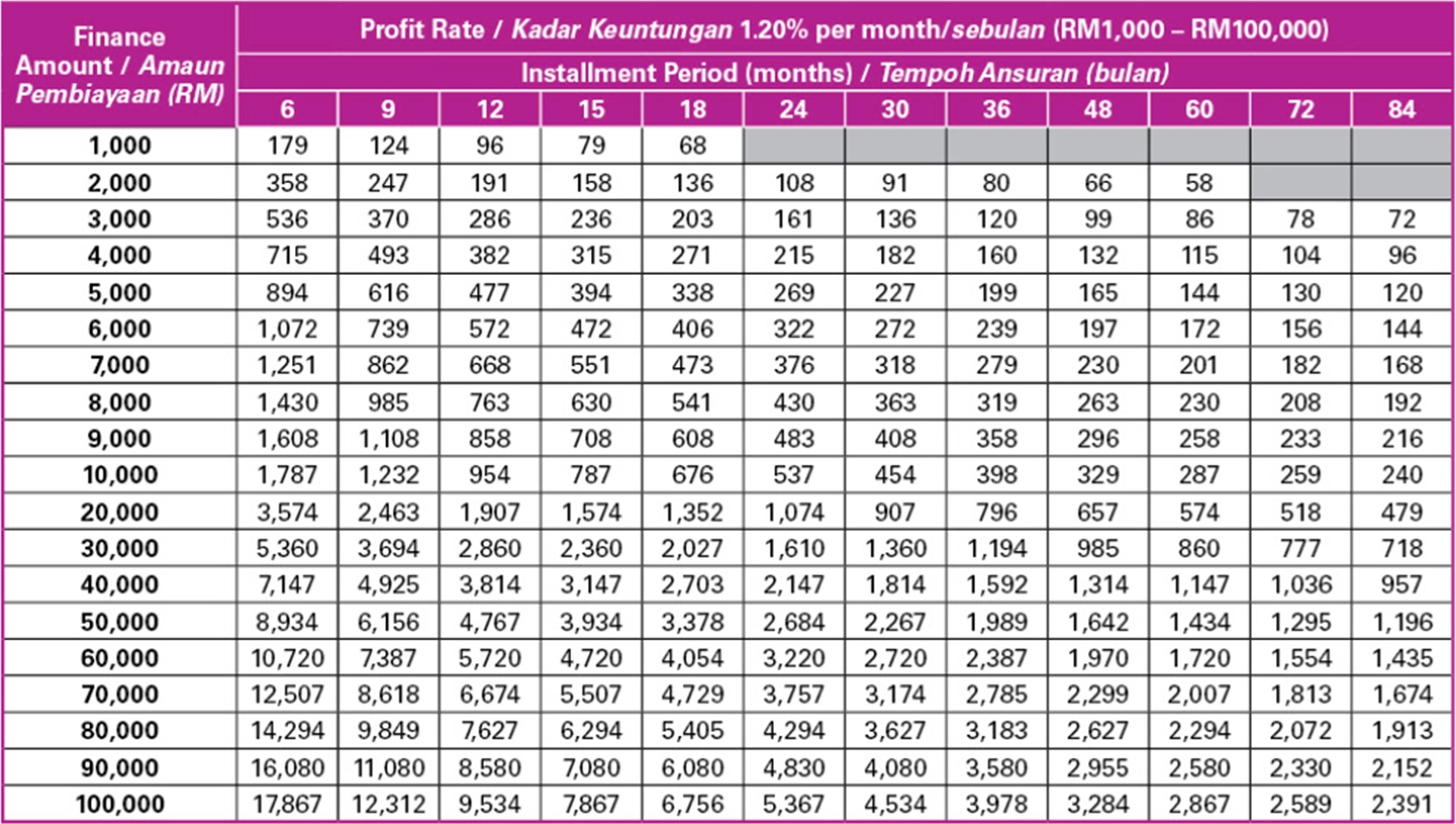

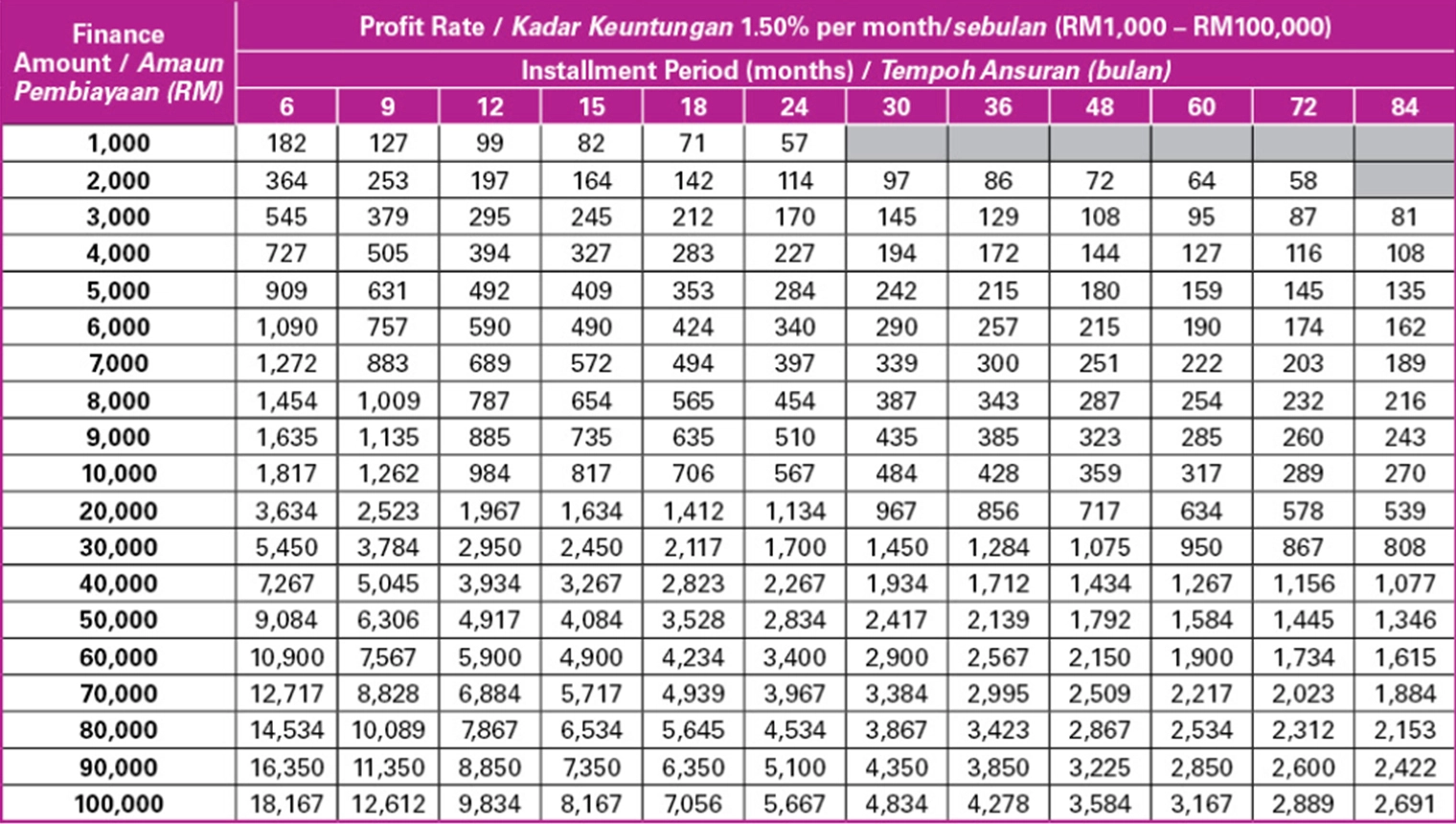

Table of Profit Rates (RM1,000 – RM100,000)

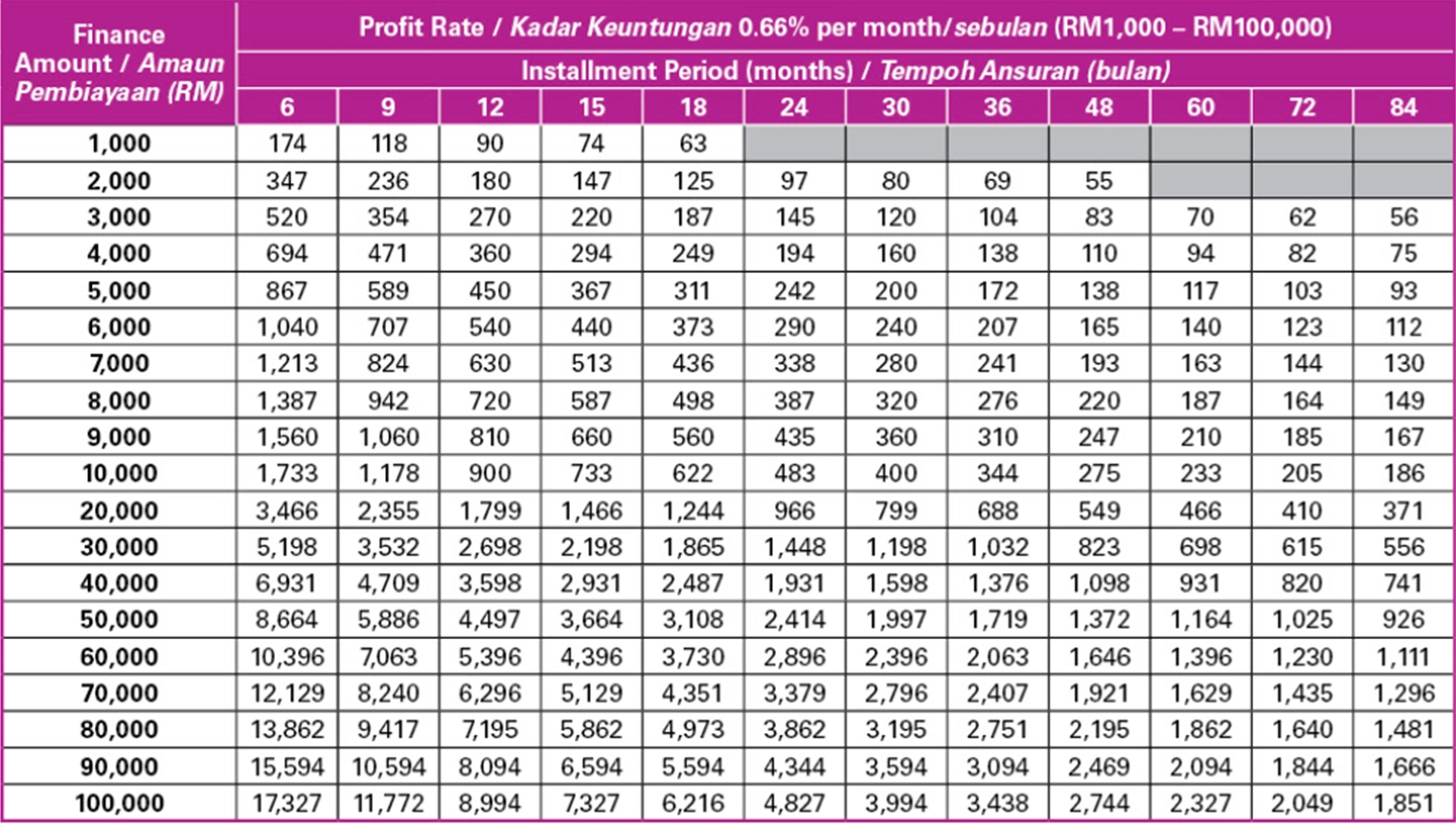

Table 1: Profit Rate 0.66% per month

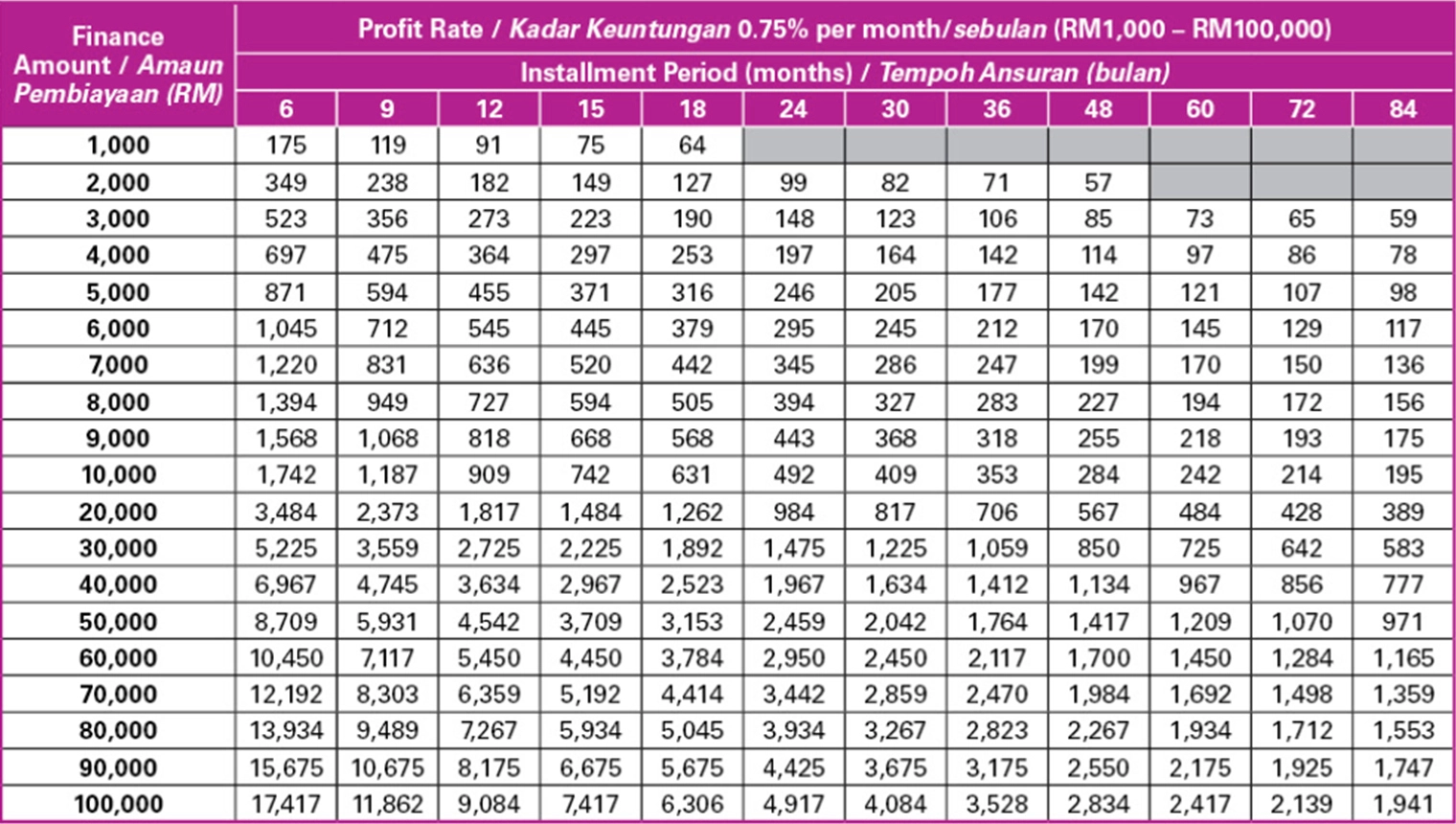

Table 2: Profit Rate 0.75% per month

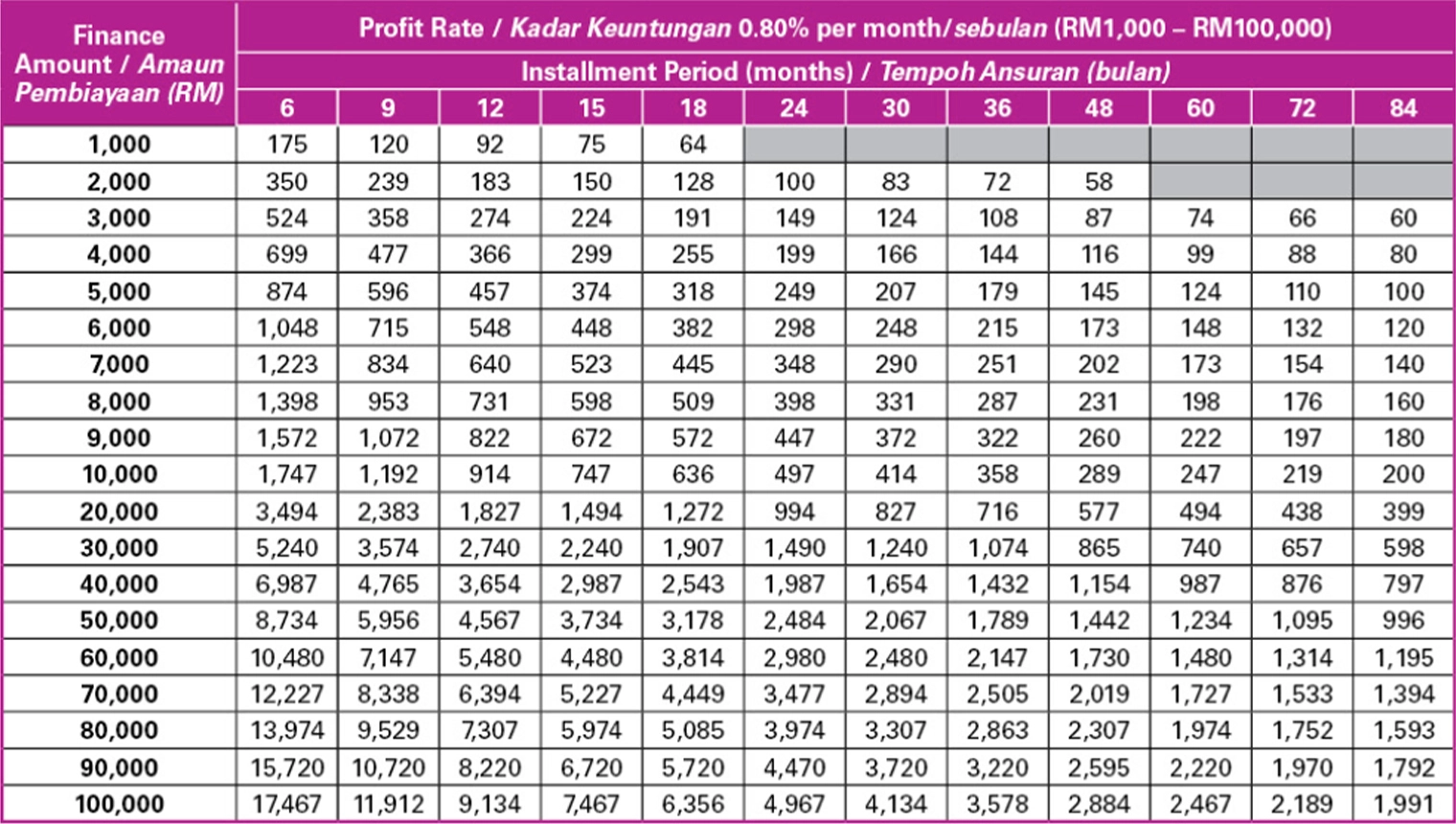

Table 3: Profit Rate 0.80% per month

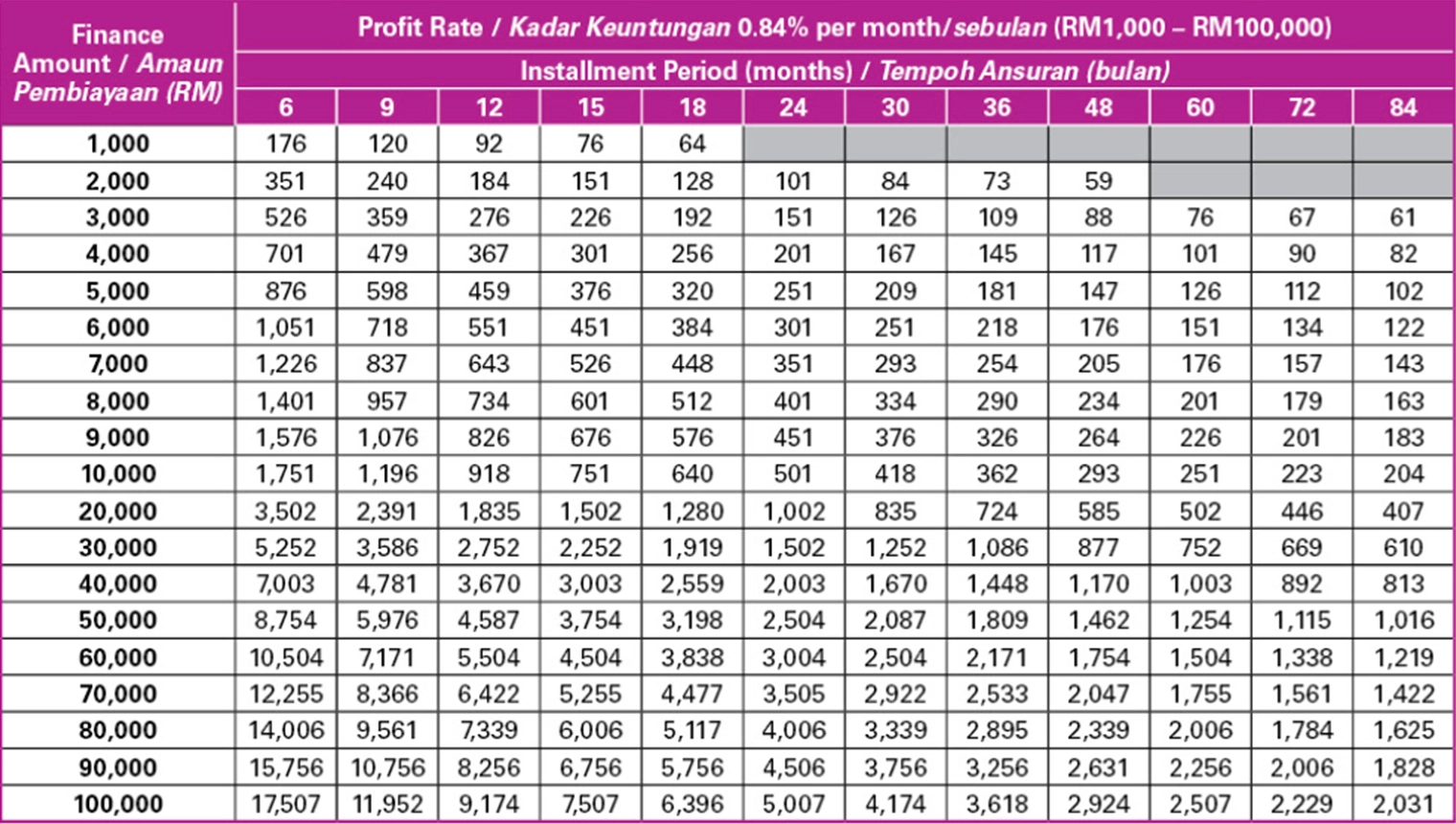

Table 4: Profit Rate 0.84% per month

Table 5: Profit Rate 1.20% per month

Table 6: Profit Rate 1.50% per month

Please note that your actual approved amount, profit rate, and tenure depend on your credit assessment and may differ from the tables above.

The profit rate is quoted as a flat (fixed) monthly rate ranging from 0.66% to 1.50% per month:

| Flat profit rate | Flat rate per year | Approx. effective rate per year (EIR) |

|---|---|---|

| 0.66% / month | 7.92% p.a. | ~13.57% – 14.31% p.a. |

| 1.50% / month | 18.00% p.a. | ~27.46% – 31.72% p.a. |

Why the effective rate is almost double the flat rate: a flat rate charges profit on the full original amount for the whole tenure, even as you pay the balance down. The Effective Interest/Profit Rate (EIR) reflects the true cost on your reducing balance. Always compare lenders using EIR, not the headline flat rate. The lowest 0.66%/month is reserved for the strongest applicant profiles; most applicants are offered a higher rate.

Source: AEON Credit Service (M) Berhad

Big 2026 Change: Flat Rate & Rule of 78 Are Being Phased Out

Bank Negara Malaysia (BNM) has finalised reforms to personal financing. For new personal financing facilities from 1 January 2027, the flat-rate method and the Rule of 78 will be abolished. Lenders must instead price on a reducing-balance basis and disclose a standard Effective Profit Rate (EIR) so borrowers can compare like-for-like. Applications above RM100,000 will also require a short financial-education module.

What this means for you in 2026: products like AEON iCASH still quote a flat rate today, so early settlement does not save as much profit as a reducing-balance loan would. If you plan to settle early or you are borrowing a large sum, this is a real cost factor — read our pitfalls section below. For context, BNM’s Overnight Policy Rate (OPR) sits at 2.75% (held at the May 2026 meeting), which anchors the wider lending market.

Benefits & Features

Here is what you get with this aeon loan:

- Fast approval with disbursement possible any day of the week — even on a Sunday

- Financing from RM1,000 up to RM100,000

- Flexible repayment tenures of 6, 9, 12, 15, 18, 24, 30, 36, 48, 60, 72 and 84 months

- Lower minimum income (RM1,500/month) than most conventional bank personal loans

- Shariah-compliant (Tawarruq) — no riba; profit is fixed and known upfront

- Unsecured: no guarantor, no collateral, and no security deposit needed

- No early-settlement penalty, with an Ibra’ (rebate) on the unearned profit if you settle ahead of schedule

Eligibility

- Malaysian citizens (private-sector employees and uniformed bodies such as police and military are accepted)

- Age from 18 up to 65 years old; note that new AEON Credit customers must generally be at least 22 (confirm with AEON Credit)

- Minimum gross income of RM1,500 per month

- Financing amount from RM1,000 up to RM100,000

Documents Required

1) Salaried Employee

| Source of Income | Required Documents |

|---|---|

| Fixed Income Earner | NRIC copy (front & back); plus latest 1-month salary slip OR latest EPF statement |

| Variable Income (Non-Commission) | NRIC copy (front & back); plus latest 3-month salary slips OR latest EPF statement |

| Variable Income (Commission-Based) | NRIC copy (front & back); plus latest EPF statement OR latest 6-month commission statement |

2) Self-Employed

| Source of Income | Required Documents |

|---|---|

| Self-Employed | NRIC copy (front & back); plus Business Registration Certificate (ROC or ROB) and any one of: latest 6-month company current-account statement OR latest bank savings passbook/statement OR latest BE/E Form & tax payment receipt |

Fees and Charges

This aeon loan carries the following fees. Most are deducted from the disbursed amount, so you receive slightly less than the approved sum — budget for this.

| Fee | Amount (2026) |

|---|---|

| Processing fee (≤ RM10,000) | 4% of financing amount |

| Processing fee (> RM10,000) | 2% of financing amount |

| Processing fee cap | Maximum RM400 |

| Stamp duty | 0.5% of the financing amount |

| Wakalah fee | RM10.80 (inclusive of 8% service tax) |

| Early termination / settlement fee | None (Ibra’ rebate applies) |

| Late payment charge | 1% per annum on the overdue amount, plus a penalty of RM18 up to a maximum of RM40 if not paid by the 10th of the month |

*The Wakalah fee rose to RM10.80 in line with the 8% service tax (previously RM10.60 at 6% SST). You are responsible for any applicable taxes. Please visit aeoncredit.com.my for the latest schedule.

Worked Example: What RM10,000 Over 5 Years Really Costs

Say you borrow RM10,000 over 60 months at a flat profit rate of 0.84% per month (10.08% p.a. flat):

- Total profit charged: RM10,000 × 10.08% × 5 years = RM5,040

- Total repayable: RM10,000 + RM5,040 = RM15,040

- Monthly instalment: ~RM250.67

- Upfront fees deducted: 4% processing (RM400 cap applies, so RM400) + 0.5% stamp duty (RM50) + RM10.80 Wakalah = ~RM460.80, so you actually receive about RM9,539

The same RM10,000 at the best 0.66%/month rate would cost RM3,960 in profit instead of RM5,040 — a RM1,080 difference over the tenure. This is why the rate you are offered matters far more than the headline “as low as 0.66%” figure. Use our personal loan calculator to model your own numbers before committing.

How to Decide If AEON iCASH Is Your Best Option

Work through these three steps before you apply:

- Check bank rates first. If you earn RM3,000+/month with a clean record, a bank personal loan (e.g. GXBank, CIMB Cash Plus, or RHB) will usually beat AEON’s effective rate. See our roundup of the best personal loans in Malaysia.

- Match the product to your situation. AEON iCASH shines when banks reject you for low income, when you need cash on a weekend, or when you want a Shariah-compliant facility. If speed is everything, compare fast-approval personal loans.

- Borrow the smallest amount over the shortest tenure you can afford. Because profit is flat, a longer tenure dramatically increases total cost. Keep your Debt Service Ratio healthy and check your credit standing first with our guide to checking your CTOS score.

Common Pitfalls to Avoid

- Confusing flat rate with effective rate. A 0.66%/month flat rate is roughly 13.6% EIR — not 7.92%. Compare lenders on EIR.

- Forgetting the upfront fees. Processing fee, stamp duty, and Wakalah fee are deducted from your disbursement, so you receive less than the approved amount.

- Over-stretching the tenure. A flat-rate facility charges profit on the full original amount for every month of the tenure, so 84 months can cost far more than 36.

- Assuming early settlement saves a lot. Under a flat-rate/Tawarruq structure the Ibra’ rebate is modest compared to a reducing-balance loan — this changes for new facilities from 2027.

- Missing the 10th-of-month deadline. Late payment triggers a 1% p.a. charge plus an RM18–RM40 penalty and can hurt your credit file.

Alternative: AEON Bank Personal Financing-i (Fully Digital)

If you prefer a completely app-based experience, AEON Bank (the digital Islamic bank, separate from AEON Credit) offers Personal Financing-i with instant disbursement straight to your AEON Bank Savings Account-i. As of 2026 it offers financing from RM1,000 up to RM100,000, tenures of 3–84 months, for Malaysian citizens aged 18–55 with a minimum gross income of RM2,500/month (gig workers and commission earners welcome). Its profit rate is personalised and quoted as an effective rate — worth comparing against AEON iCASH if you want a paperless application. Confirm current terms on the AEON Bank website.

*Tip: To compare AEON iCASH against other lenders, read our guide to the Best Personal Loans in Malaysia, or if you bank with CIMB, our CIMB Cash Plus review.

Frequently Asked Questions

Disclaimer: This article is provided by KayaToday for general information only and is not financial advice. Profit rates, fees, and eligibility were verified in June 2026 but can change at any time — always confirm the latest terms directly with AEON Credit Service (M) Berhad before applying.